Different Yield Concepts You Need to Know

Coupon vs Yield to Maturity (YTM)

Coupon rate calculates fixed and guaranteed interest payments set at issuance or based on face value, while the bond’s yield (total annual return) fluctuates depending on the bond’s current market price. Coupon remains constant during the maturity of a bond while the yield changes based on market demand and supply. Coupon is cash income, and yield shows a total return.

For example, If the annual coupon rate is 3% of $1,000 face value, the coupon will be $30 per year. Yield is an actual return, where you buy the bond at $900, the yield will be higher than 3% as the bond price is lower and you gain the difference at maturity.

Yield to maturity estimates a total return on a bond when the bond is held to maturity, factoring in the current price of the bond and interest reinvestment. In order to raise yield to maturity of existing bonds, the price must be lower than the face value. Also, in a rising interest rate environment, competitive bonds will be issued at a higher yield, which will affect existing bonds’ YTM.

Real Yield

Real yield is inflation-adjusted annual return representing true growth in purchasing power. You can get real yield by subtracting inflation rate from the nominal yield. If a bond has 5% nominal yield and inflation is 2%, the real yield will be approximately 3%.

Real Yield = Nominal Yield – Inflation Rate

When the real yield is positive, the investment grows faster than inflation which represents increase in wealth, while a negative real yield is indicative of a loss in purchasing power which does not keep pace with the rising prices. Rising real yield can be associated with expectations of robust economic growth and a decline in real yield indicates investors expectation of a weaker real growth in the economy.

Real yield can be an important indicator for financial market. Nominal interest rate can fluctuate, but the real yield derived from Treasury Inflation-Protected Securities (TIPS, inflation-protected US government bonds) can provide clearer indication of the market. It is one of the most important drivers of valuation in many asset classes as well. Falling real yields can often point to subdued macro-economic outlook, as investors expect lower real returns and will increase demand for safe investments.

Bond Equivalent Yield

Bond equivalent yield is non-compounded annual return used to compare different bonds, for example, when comparing short-term discount bonds vs semi-annual coupon-paying bonds. It allows investors to compare yields across different bonds with varying maturities and payment structures.

Term Premium

Term premium is a risk premium investors demand for holding longer-dated bonds. It can rise in response to high government debt issuance volumes, fiscal uncertainties and geopolitical risks.

How Does Interest Rate Affect Bond Price?

Bond prices and interest rates move in an opposite direction. When the interest rate rises, bond prices fall and when interest rate falls, bond prices rise. Imagine that you buy a bond paying a fixed 4% interest rate. If a new bond issued offers 5% in a month, your 4% bond now looks less attractive to other investors. To sell it, you would have to lower the price. Conversely, if rates fall to 3%, then your 4% bond becomes more valuable and you can sell it for a higher price.

What Are Duration and Convexity?

Duration and convexity are used to manage the risk exposure of fixed income investments. Duration measures the sensitivity of a bond to interest rate changes and convexity measures the curvature of the relationship between the bond price and interest rate.

What Is Duration?

Duration is one of the factors bond investors consider when assessing a bond’s investment risk. Duration quantifies the sensitivity of a bond to the changes in interest rate. Duration indicates how far the bond price would rise or fall if interest rates fall or rise. In general, bonds with a higher duration will increase in value than bonds with a lower duration in a falling interest rate environment. When you expect interest rates to go down, it will be beneficial to extend the duration of the portfolio. Duration of a portfolio can change as some of the bonds in the portfolio mature and interest rates in the market change.

Time to maturity and coupon rate of a bond are factors that influence a bond’s duration as well. The longer the maturity, the higher the duration and hence the greater interest rate risk and the reward from higher bond prices. The higher coupon rate will lower the duration and hence lower the interest rate risk.

How Does the Change in Interest Rate Affect the Duration?

When the interest rate in the market rises, duration decreases, and when the interest rate falls, duration increases. This happens because of the timing of cash flows (coupons) interact with the new interest rate environment. Bond prices trade based on the present value of future cash flows. When the interest rate (discount rate) changes, the weight of those cash flows in the calculation also changes.

When the interest rate rises, future cash flows become less valuable today because you could be investing at the new, higher rate. The bond becomes more reliant on the early coupon payments to provide value to the investor as the final principal repayment will be heavily discounted. Because the bond pays you back relatively sooner via higher-weighted earlier coupon, the effective time you wait to get your money decreases, and therefore duration goes down.

Conversely, when the interest rate falls, future cash flows become more valuable today. The big principal payment at the end becomes extremely attractive compared to the smaller coupon payments. The bond becomes more reliant on the final lump-sum payment to provide value and the earlier coupons become less significant. As the bond’s value is tied up in that principal payment, the effective time you wait to get your money increases and therefore, duration goes up.

What are the different types of Durations?

There are several ways to measure durations.

Macaulay duration

Macaulay duration measures how long it takes (in years) for an investor to be repaid a bond’s price through its total cash flows. This duration calculates the weighted average length of time or maturity expressed in years that takes for an investor to receive the bond’s present value based on the expected future cash flows of the bond including the principal and interests.

Macaulay Duration = sum of time-weighted present value of the cash flows / price of the bond

Here’s an example:

There is a 5-year bond with $1,000 face value with an annual coupon rate of 4%. Current market rate of interest is at 4.5%.

Present value of cash flows is as follows:

Year 1: 1,000 * 0.04 / (1+0.045)^1 = 38.28

Year 2: 40 / (1.045)^2 = 36.63

Year 3: 40 / (1.045)^3 = 35.05

Year 4: 40 / (1.045)^4 = 33.54

Year 5: 1,040 / (1.045)^5 = 834.55

Sum of all the present value of the cash flows is 978.05.

Present value of time-weighted cash flows is as follows:

Year 1: 1 * [1,000 * 0.04 /(1+0.045)^1] = 38.28

Year 2: 2 * [40 / (1.045)^2] = 73.26

Year 3: 3 * [40 / (1.045)^3] = 105.16

Year 4: 4 * [40 / (1.045)^4] = 134.17

Year 5: 5 * [1,040 / (1.045)^5] = 4,172.75

Sum of all these cash flows is 4,523.61. As a result, Macaulay duration will be 4,523.61/978.05 = 4.63 years.

Modified Duration

Modified duration is a common measure of interest rate risk and a slightly more precise measure of price sensitivity. It measures an expected change in a bond’s price given 1% change in interest rate (yield to maturity). It gives the percentage change in the bond’s price per basis point. Modified duration converts the Macaulay duration to measure how much the bond price will rise or fall when there is 1% change in the yield to maturity.

Modified Duration = Macaulay Duration / (1+ Yield/n)

Yield refers to the bond’s yield to maturity compounded periodically and n refers to the number of coupon periods per year (ex. 1 for annual payment, 2 for semi-annual payment, 12 for monthly payment, etc).

Based on the above example, modified duration will be: 4.63 / (1+0.045/1) = 4.43. It means that when there is a 1% increase in yield, the bond price will decrease by 4.43% [% bond price change = -1 * Modified Duration * Change in Yield].

Effective Duration

Effective duration shows the approximate % change in a bond’s price relative to a percentage point change in yield. Effective duration can be used for bonds with embedded options which can affect a bond’s value.

Effective Duration = [Bond Price (in down rate scenario) – Bond Price (in up rate scenario)] /( 2 * Change in Yield *Original Bond Price)

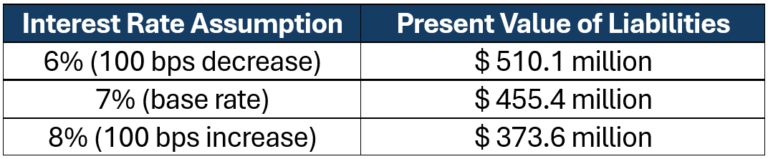

Let’s suppose a pension fund manager wants to measure the sensitivity of the pension liabilities to the market interest rate changes. The manager determined that the present value of the liabilities under three different interest rate scenarios:

The effective duration of the pension fund’s liabilities will be (510.1-373.6) / (2 * 0.01 * 455.4) = 14.99. For a 1% increase in interest rates, the liabilities are expected to fall by approximately 14.99%.

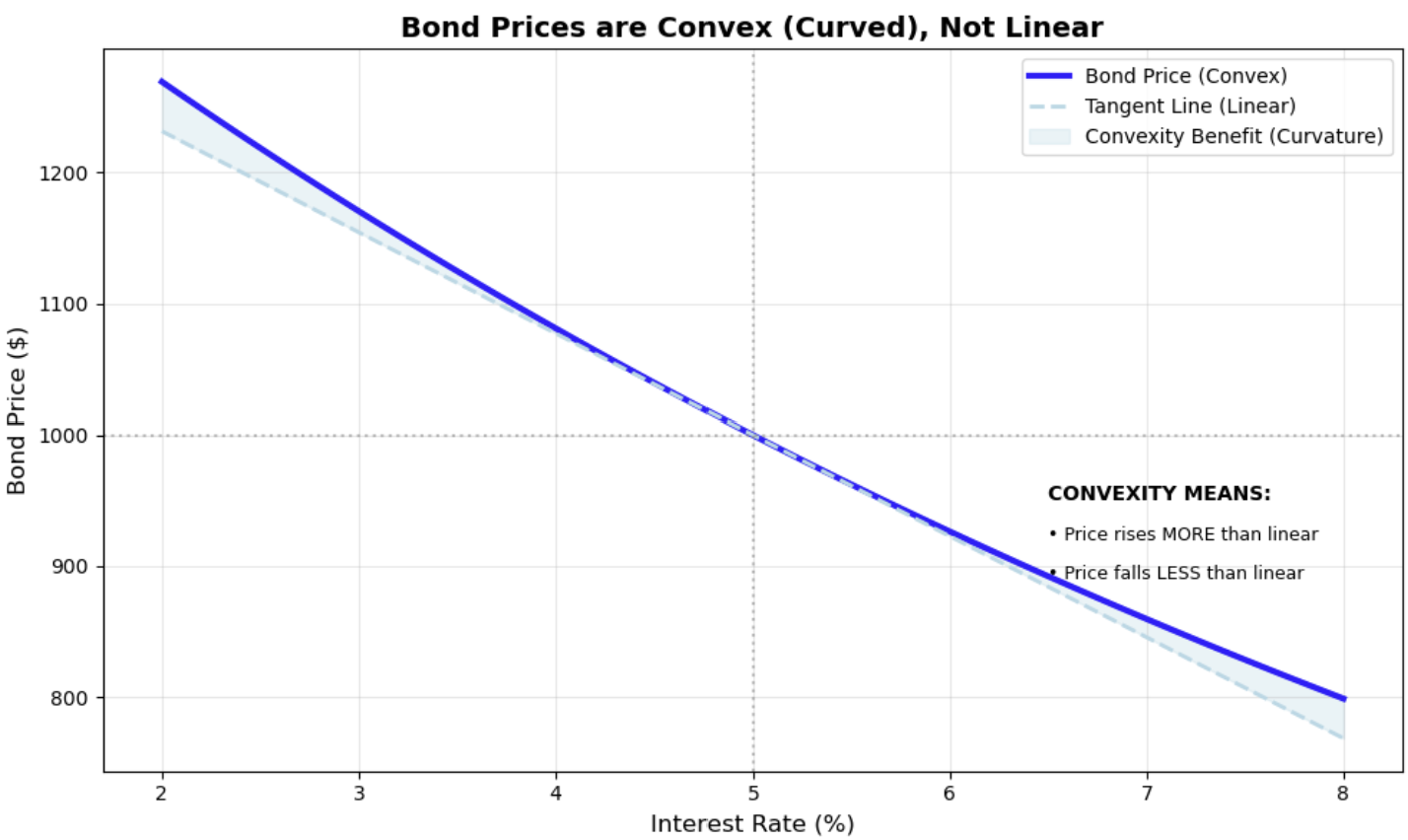

What Is Convexity?

A bond’s price and yield relationship is not a straight line but curved, convexity measures how much duration changes as yield moves. In most of plain vanilla bonds, convexity is positive, which creates desirable asymmetry when investing in bonds.

When interest rate falls, the bond price goes up faster than what the duration predicts. When interest rate rises, convexity helps the bond price to go down slower than what the duration predicts.

A bond with high convexity will be more sensitive to interest rate changes than a bond with low convexity. The more convex, the more the bond will gain in value when interest rates fall and less loss in value when interest rate rises. High convexity means more potential upside when the interest rate comes down, and more downside cushion for your losses when the interest rate goes up. Therefore, high convexity bonds will experience smaller swings in response to interest rate changes. Convexity does a better job than duration alone to estimate impact of yield changes on the bond price.

Negative curvature happens for callable bonds when the issuer has an option to repay the bonds. This means the duration of a bond will decrease as the yield decreases. This is because there will be higher demand from issuers to call the bonds and re-issue bonds at lower yields.

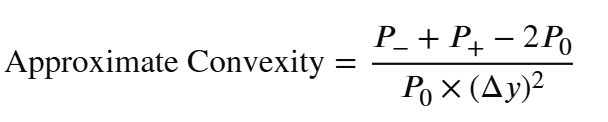

Bond Convexity Calculation

Convexity offers a more precise measure of bond price changes than duration alone when the yield shifts. The following example shows how convexity is calculated and how to apply it to estimate the bond’s new price.

Consider a bond with the following characteristics:

Face value: $1,000

Coupon rate: 5% (annual)

Time to maturity: 10 years

Current yield to maturity (YTM): 8%

Change in yield: 1%

Calculate the current bond price given 8% YTM: Bond price (P0) = $798.70

Determine the new bond price when the yield changes by 1%:

Lower yield price (P-) = $859.53 (When the YTM decreases by 1% to 7%)

Higher yield price (P+) = $743.29 (When the YTM increases by 1% to 9%)

Using the above formula, approximate convexity will be:

(859.53+743.29-2*798.70)/(798.70*(0.01)^2) = 5.42/0.07987 = 67.86

A convexity of 67.86 means that the price-yield curve is convex so when the yield falls, the bond price will rise more than what the duration predicts while when the yield rises, the bond price will fall less than what the duration predicts.

When the bond has a modified duration of 7.0, and convexity of 67.86, if the yield decreases by 1%, you can predict the percentage price change for the bond using the following formula:

Duration Effect = -7.0 * (-0.01) = 0.07 (+7%)

Convexity Adjustment: 0.5 * 67.86 * (-0.01)^2 = 0.0034 (+0.34%)

Total Predicted Change: 7% + 0.34% = 7.34%

Without convexity, we would have assumed a 7% increase in price. But as the bond has positive convexity (when the interest rate falls, the price rises faster while when the interest rate rises, the price falls slower), the price increases more (7.34% instead of 7%). A bond with a higher convexity will experience a higher price increase or lower price decrease compared to a bond with lower convexity for a given change in yield.