What Is Credit?

Credit refers to bonds issued by corporations as opposed to those issued by risk-free government. Within this space, investors aim to earn stable returns from contractual interest payments that can offer lower volatility compared to stocks. The main sources of the returns for credit bonds include: 1) Income – you collect the steady stream of interest payments, 2) price appreciation (capital gains) – The price of a bond can go up or down before it matures. You can potentially sell the bond for more than what you paid for but this is often a secondary goal to credit investors as they are usually more focused on the steady income stream.

Government Bonds vs Corporate Bonds

Government bonds fund public spending. Sovereign debts are perceived as low risk as government can raise taxes or print money to repay the debts. However, inflation and political instability can be risk factors. Corporate debts usually fund company’s operations and risks are tied to business performance and profitability. Companies need to provide extra yield over a risk-free government bond to compensate for higher risk and this is called credit spread.

Some of the companies are not considered less risky than their own governments. This is a phenomenon as the governments have borrowed heavily since the pandemic with rising debt-to-GDP ratio. In contrast, companies like Microsoft (AAA-rated, higher than US government’s credit rating of AA+) can use their strong earnings to pay down the debts. It has little debt and it can yield less than US Treasury bonds. Investors can compare corporate balance sheets versus government’s fiscal policies to make more sound investment judgement. Investors should decide if the credit spread, extra yield from the corporate bonds compensates the risk, especially in a market where the government yields are also moving.

What Is Credit Spread?

Credit spread is the extra yield an investor demands to hold a risky corporate bond over a risk-free government bond. Credit spread, the difference between the yield for credit bonds and that for safer government bonds can provide a signal that investors are taking on more risk. A wider spread shows more caution.

Change to a credit bond’s yield can come from the change in the market interest rate or from company-specific change such as improving or worsening credit profiles. Credit spread, however, may not be a good leading indicator as they get widen after things get serious in the financial market. Credit spreads can widen due to higher supply in the issuance market. More equity issuance can provide safety net to bondholders.

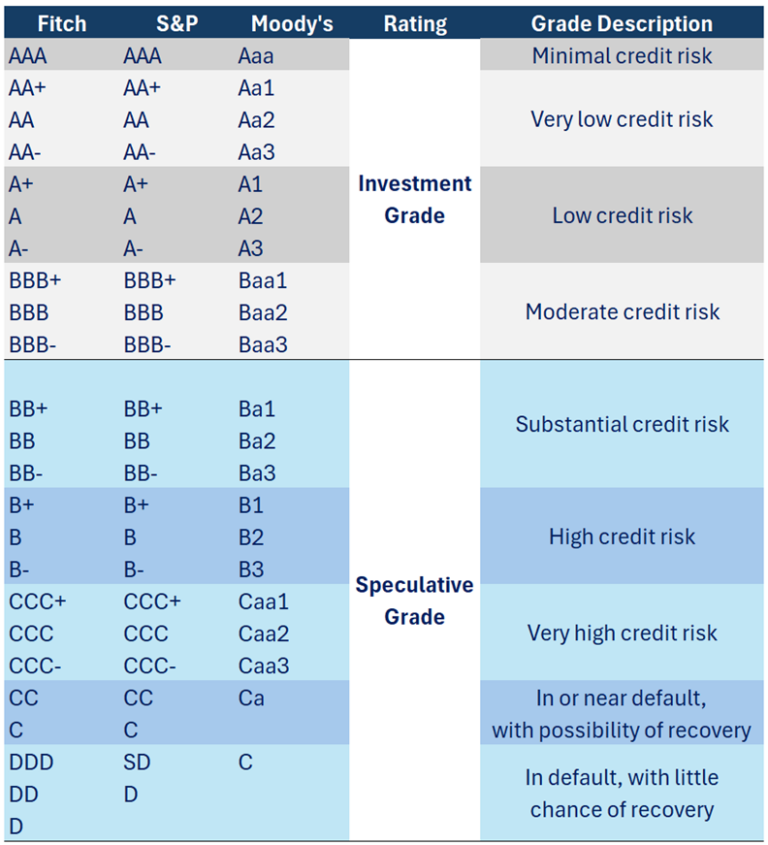

What Is Credit Rating?

Credit Rating is given by rating agencies such as S&P, Moody’s and Fitch that estimate the borrower’s ability to repay. It’s like a credit score for governments and companies. Investment grades are with high quality and low risk of default and are ranging from AAA to BBB-. High-yield or junk bonds are lower quality bonds with higher risk of defaults. As a result, they provide higher interest rates to compensate for higher risks investors are taking. In the worst case scenario, default happens when the borrower fails to make a payment on the interest or the principal.

What is Credit Analysis?

Credit analysis is about answering one question: will this borrower pay me back on time and in full? It is the process of evaluating a borrower’s ability to repay debts focusing on risk factors, repayment capacity and financial resilience. It combines qualitative analysis on the management quality and governance (strategic decision-making, transparency, reputation – borrower’s willingness and capacity to honour obligations), industry and macro-economic conditions (competition, cyclicality and regulation) with quantitative analysis of financial statements. Key quantitative ratios include debt-to-equity, debt-to-asset for leverage, current ratio and quick ratio for liquidity, and interest coverage and debt service coverage ratio for coverage.

What are 4Cs?

Character: It examines a borrower’s reputation, track record (a firm’s history of honouring obligations) and willingness to repay.

Capacity: It checks a borrower’s ability to generate cash flow to service its debts. Can a company afford the new debt payments after covering all the operating expenses and existing debt-related payments (interest and principals due)? Debt Service Coverage ratio (DSCR: Net Operating Income / Total Debt Service [Principal+Interest]) helps to analyse it. A ratio above 1.20x or 1.25x is a common minimum benchmark, meaning that the company generates 20-25% more cash flow than what’s needed for the debt payments.

Capital: It measures the borrower’s financial cushions – how much of their own money has the company invested? Look at the Leverage Ratios (Debt-to-Equity ratio). Higher ratio signals the company is funded aggressively by the debts, leaving a thin cushion for the lenders.

Collateral: Collateral refers to assets pledged to secure loans. If the borrower defaults, lenders can seize and sell the assets (such as real estates, equipment or account receivables) to recover the funds. A critical metric to measure this is Loan-to-Value ratio (LTV: Loan amount / Appraised Value of Collateral) and the lower the ratio the safer it is.

Credit Analysis Checklists

Business profile: Does the company in a cyclical or defensive industry? Does the company have competitive advantages (strong customer base, brand value, etc) with a strong market position? How’s the management quality (governance, transparency, track record)?

Purpose and sources of repayment: Define the loans intent and identify the primary and secondary repayment sources. Generally, ongoing operational cash flow will be the primary source of repayment and liquidation of collaterals or a new investor’s capital injection will be a secondary source of repayment.

Debt Structure: How’s the maturity profile (near-term or long-term obligations)? Is it secured or unsecured debts? Which currency does the debt is denominated in (measuring FX risk)? Does the company have any off-balance sheet liabilities (leases, guarantees)?

Financial analysis (Financial risk): 1) Profitability: Is the business viable long-term? (gross margin, net margin, return on assets), 2) Liquidity: Can it meet short-term obligations? (current ratio: current assets / current liabilities, quick ratio: (current assets – inventories) / current liabilities), 3) Leverage: How much debts does a company have versus equity? (debt/equity, debt/EBITDA), 4) Coverage: This measures debt servicing capability (debt service coverage ratio: net operating income / total debt service [Principal+Interest]), interest coverage ratio: operating income or EBIT / interest expenses)

Cash flow Analysis: The essence of cash flow analysis is analysing free cash flow (FCF: Cashflow from Operation – Capital Expenditures). This is discretionary cash available to pay down debt principal after maintaining the business operation. Strong and consistently positive FCF warrants high-quality credit.

Structuring and Documentation: The final step is structuring a loan to mitigate the identified risks. Terms and covenants can be documented in the credit agreement. Terms include maturity date, interest rate (fixed or floating) and repayment schedule. Covenants refer to rules that borrowers must follow. Affirmative covenants require actions such as providing annual audited financials, negative covenants restrict actions such as unable to take on more debt without lenders’ permission, and limitation on dividend distribution.

External Factors: Examine macro-economic environment (interest rate and inflation), regulatory risk (compliance, legal disputes) and country risk (political stability, sovereign rating).