Bond Investment Strategies

Bond investment can provide diversification within the portfolio while generating regular income. As the bond price moves inversely to interest rates – bond price rises when the interest rate falls, the bond investment strategy should be designed to manage interest rate risk, reinvestment risk and credit risk.

What Are the Core Bond Investment Strategies?

You can choose bond investment strategies aimed to provide steady income stream, protect capital and manage reinvestment risk.

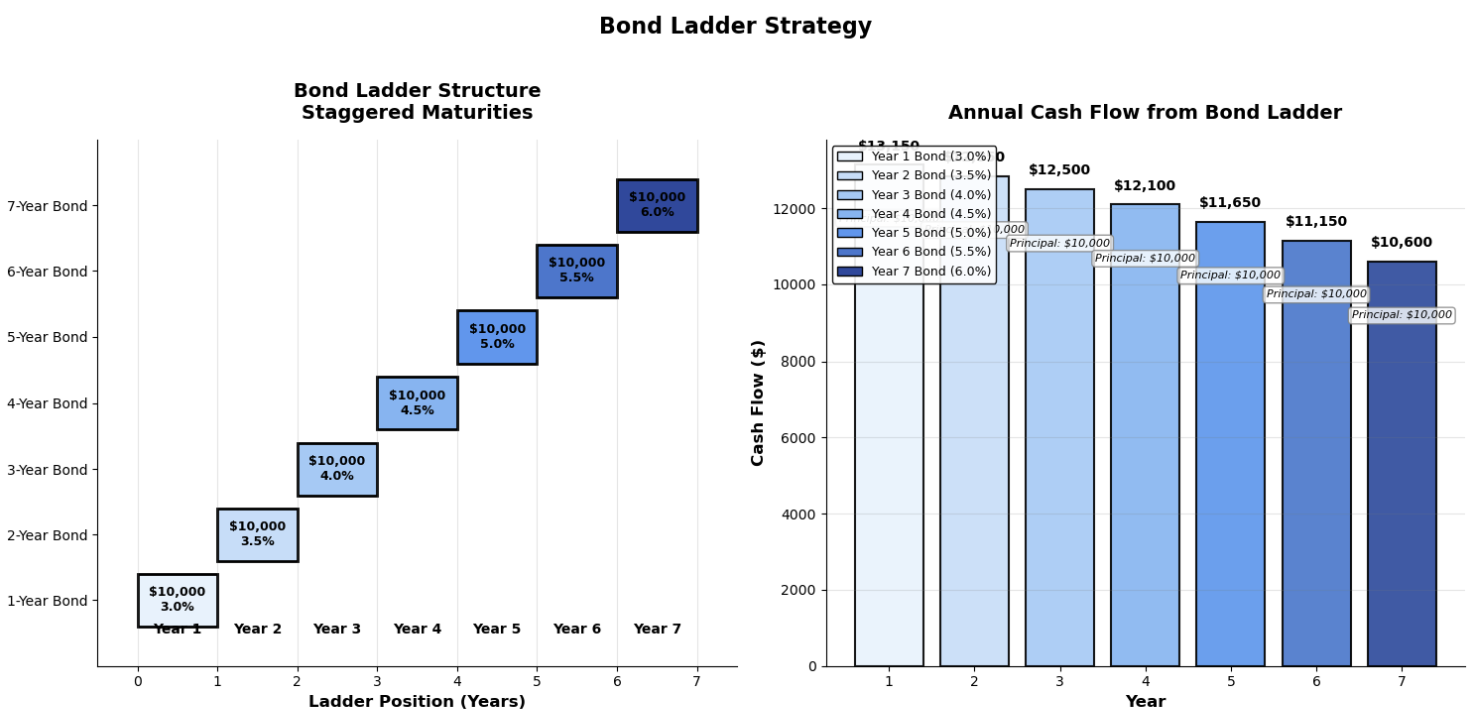

Ladder strategy

This strategy involves buying multiple bonds with staggered maturity dates. For example, buy bonds maturing in 1 throughout to 10 years. As each bond matures, the proceeds are reinvested in a new long-term bond, balancing yield with liquidity. This will provide consistent cash flows and reduce the risk of reinvesting all capital in a low-rate environment. This strategy provides income and stability.

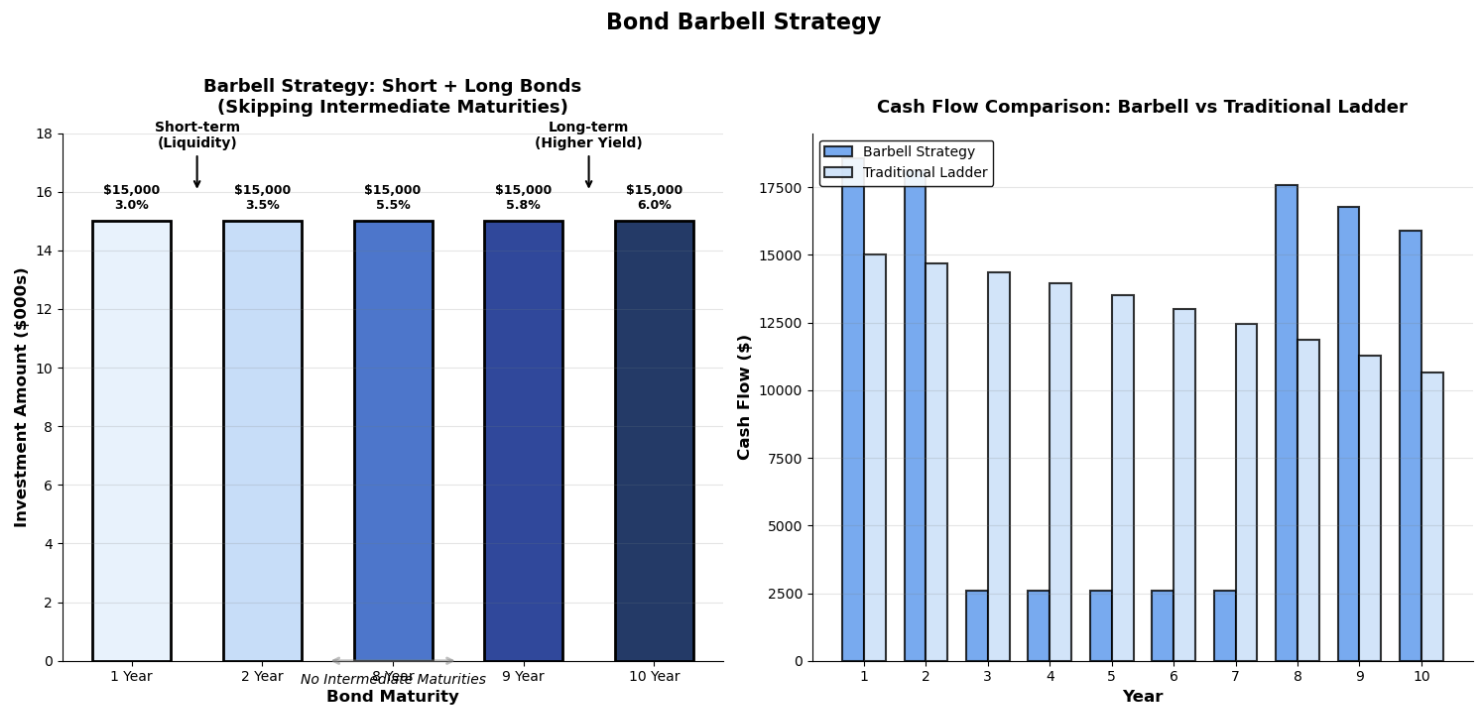

Barbell strategy

This strategy consists of purchasing bonds at the two extremes of the yield curve – short-term bonds for liquidity and long-term bonds for higher yields. This allows investors benefit from higher yields while retaining flexibility from the short-term bonds, which can be reinvested when the interest rate rises.

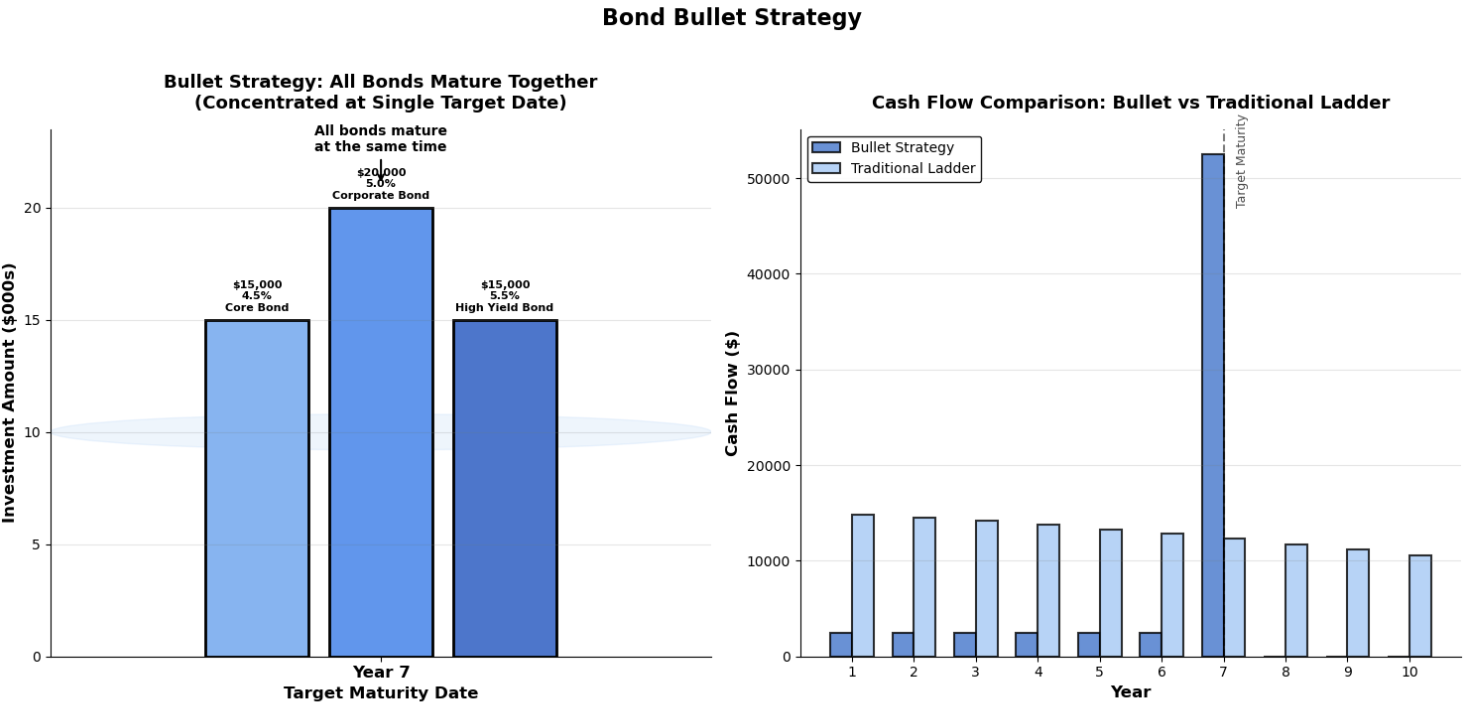

Bullet strategy

This strategy involves purchasing bonds that fall within a similar timeframe such as bonds all maturing in 5 years. It targets a specific maturity date. It is ideal for funding a specific future goals or liabilities such as a house or university tuition.

Buy-and-hold strategy

Without affected by short-term price fluctuations or volatility from interest rate changes, investors buy and hold the bonds until maturity to receive the full principal back.

Long/Short credit

This is a hedge fund strategy whereby taking long positions in undervalued credit and short positions in overvalued credits to profit from any price fluctuations in the market.

What Is Active Bond Management?

Active bond management aims to outperform a bond index by trading based on interest rate forecasts and bottom-up credit analysis. Passive strategy, however, involves buy and hold a diversified bond portfolios using index funds or ETFs in order to match the performance of the benchmark index.

Duration management

Active managers adjust duration – interest rate sensitivity of the portfolio. When the interest rate is expected to rise, investors can reduce the portfolio duration by selling long-term bonds and buying short-term bonds. Or buying floating-rate notes, or TIPS (Treasury Inflation-Protected Securities) can be another option as well. Conversely, in a falling interest rate environment, lengthen the duration by buying long-term bonds.

Yield curve positioning

Investors can consider a barbell strategy when higher long-term rates are anticipated to take advantage of higher long-term rates and re-investment of short-term bonds for liquidity.

Liability matching

Matching the duration of bonds to that of future liabilities such as retirement expenses can be another active strategy to ensure required cash is available regardless of any interest rate changes.

How to Choose A Strategy?

Conservative investors focus on short to intermediate-term government bonds or high-quality investment-grade corporate bonds to prioritize capital preservation. Income seekers will prefer ladder strategy, look for high-yield corporate bonds or emerging market bonds with higher credit risks compared to developed market bonds. Tax-sensitive investors will focus on municipal bonds which can be tax-exempt at federal or states levels.