How Does Geopolitical Risk Impact Asset Classes?

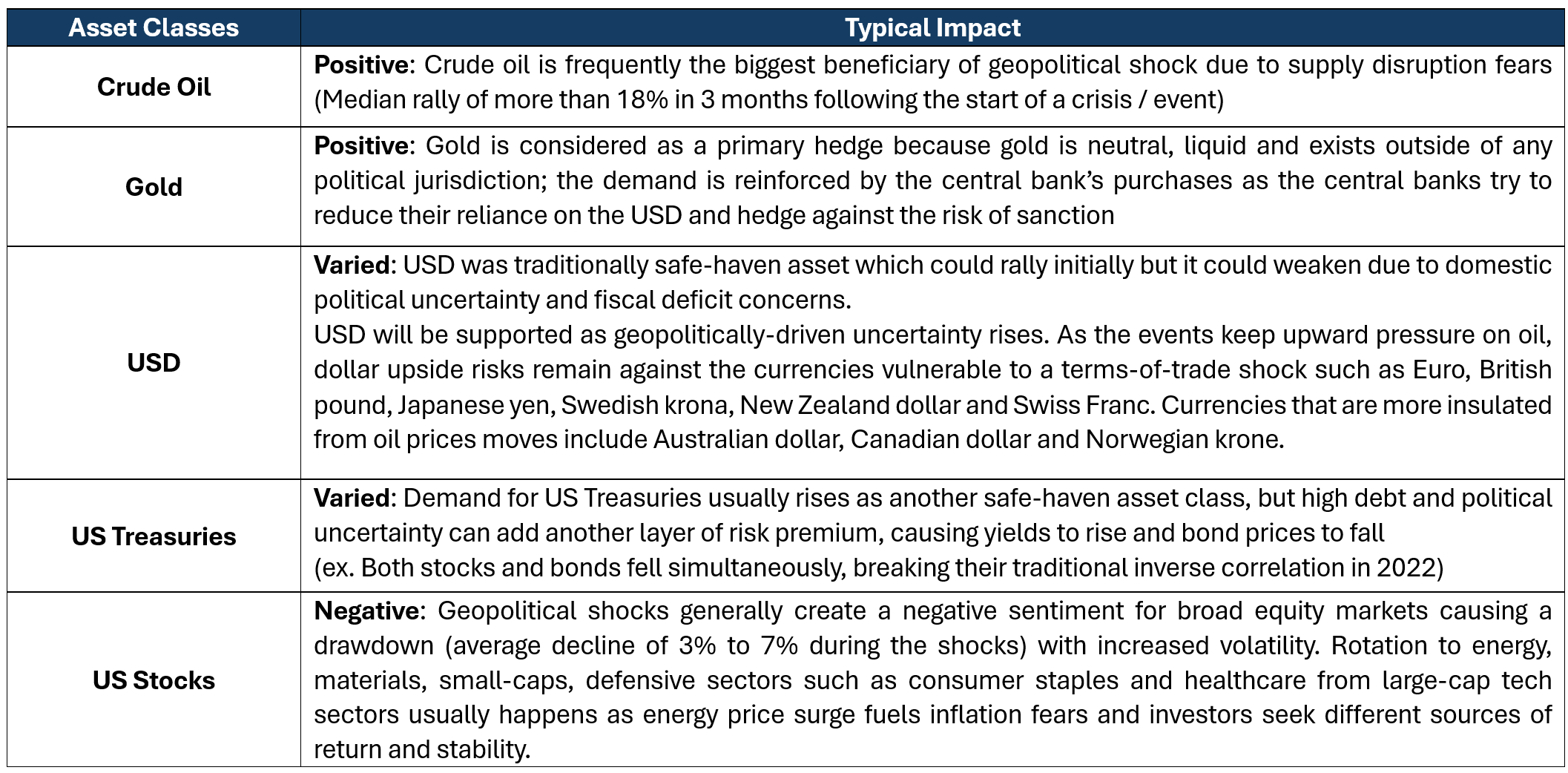

Geopolitical risk impacts asset classes by triggering investors behavior – flight to safety. Generally, traditional safe havens such as gold and US dollar benefits from geopolitical tensions.

The primary driver of price action in early March 2026 was geopolitics – the broadening conflict between Israel, Iran, and the US. Investors remain on high alert for further escalation in the Gulf region. Domestic economies around the world will be tested if they can remain resilient in the face of soaring energy prices and global instability caused by geopolitical risk.

Commodities, especially oil surged, US equity indices were in the red and Treasuries saw two-way trade settling mostly flat as investors weighed safe-haven demand versus inflationary fears. Classic geopolitical risk-off sentiment favors dollars.

The

current environment — marked

by an energy supply shock fuelling both inflationary pressures and recession concerns

— underscores that

stocks and bonds may not exhibit the negative correlation investors have come to

rely on. Less correlated assets such as gold, commodities and infrastructure warrant

greater consideration to boost portfolio resilience amid ongoing conflict and

its economic repercussions continue to unfold.

The key issue is the duration of the shock as the market quickly gets used to a situation that can last weeks or months. Diversification is the key. No single asset is a perfect haven in every scenario. A resilient portfolio would be combining assets that can react differently to various shocks. A combination of the stock indices, bonds and commodities such as gold can be effective for mitigating downside risks arising from geopolitical shocks over the longer horizon.

US Treasury yields have moved higher across the curve in anticipation of higher inflation that got elevated due to oil prices. Inflation makes holding longer duration bonds less attractive and higher yields make holding gold more expensive on a relative basis. It seems like oil and USD are the only attractive safe haven assets to hide out during this Middle East geopolitical tension. A stronger dollar pressured commodity prices including precious metals making them more expensive for foreign buyers. When the yields remain elevated and the USD stays firm, US Treasuries can offer as a compelling alternative. However, if growth weakens and central bank pivots back toward easing, gold can look attractive again as a long-term store of value and a safe haven asset.

How Does Iran Oil Shock Compare to 1997 Asian Financial Crisis for Emerging Economies?

Asian financial crisis in 1997 was driven by a mixture of fixed exchange rates, high levels of short-term foreign debts, low levels of foreign exchange reserves and high current account deficits. But Asian economies these days are much better protected with more flexible exchange rate regimes and larger foreign exchange reserves providing a buffer to absorb the oil shock. Asian economies now also have deeper local financial markets with broader domestic investor base and less reliance on short-term foreign funding, which reduces the risk of sudden capital flight and forced deleveraging happened during 1997 crisis. The 1997 crisis was about a shock to the financial account with bank inflows dried up, while current crisis is more about a supply shock to the current account with reduced oil product inflows.

In the late 1990s, many Asian countries held large amounts of USD-denominated debts. It made the economies vulnerable when the local currency got weakened. Now, however, most countries have built up their USD reserves, which allows central banks to safeguard their currencies, and allow their currencies to move more freely, thereby enabling them to absorb pressure by gradually weakening their local currencies and reducing the risk of collapse in defended peg system. During the current oil shock, ample USD reserves allow central banks to avoid having to hike rates aggressively to defend their currency peg.

Emerging market currencies can come under pressure when this oil shock gets prolonged and oil price remains elevated for longer. In addition, when emerging economies sell Treasuries to raise USD in an effort to defend their currencies, this selling pressure can push US yields higher and can create a ripple effect through global bond markets. Emerging economies are generally more vulnerable to US yields spikes. When the US yield spike is driven by term premium (demand for higher compensation for holding longer-term bonds), dollar appreciation, and elevated emerging market inflation expectation, these conditions will prompt emerging market rate hikes.

How Does the Geopolitical Risk Affect Different Currency Pairs?

During recent Iran conflict, crude oil and the US dollar rose together breaking a long-standing market relationship forcing investors to adjust. Normally, a stronger dollar weighs on oil because it makes crude oil more expensive for foreign buyers, which reduce demand for it. But when both move higher at the same time, it means geopolitical supply risk, resilient global growth, or safe haven demand for dollars is driving the market. Commodity-linked currencies may not weaken as much as they normally would against a stronger USD because higher export revenues can provide support. In rates, higher energy prices can keep inflation expectations sticky, reshaping yield curves and central bank expectations. When oil and the USD rise together, cross-asset volatility usually increases, which could trigger position unwinds and force investors to rely less on historical relationships, and more on the real-time drivers.

Historical oil supply shocks tend to benefit US dollar and Canadian dollar. Oil producing economies generally see their currencies outperform, while currencies of energy-importing countries particularly like Japan, China, and across Europe underperform, as they are more dependent on Persian Gulf supplies and their currencies often weaken. Yen occasionally weakens during oil shocks reflecting Japan’s heavy reliance on imported energy. However, it can be offset by the traditional safe-haven flow during periods of market stress.