Equity Investment Strategies

Major equity investment strategies can be categorized by investment style (value investing – finding undervalued stocks, growth investing – targeting high-growth companies, momentum investing – betting on the recent trends by buying securities that have performed well recently and selling those that have performed poorly), by level of activeness (passive investing – buying an index for the broad market exposure, active investing – selecting securities through top-down macro analysis or bottom-up fundamental research).

The followings provide a detailed overview of key equity investment strategies.

Value Investing: It identifies stocks trading below their intrinsic value, looking for a potential for price correction. Look for low P/E, Low P/B and high dividend yield. This strategy hinges on the fact that market is emotional and price will eventually reflect its intrinsic value.

Growth Investing: This strategy buys companies that are expected to grow their revenues or earnings faster than the market average even if the stock price appears to be high relative to the current fundamentals. Look for companies with high revenue growth, high EPS growth, or PEG ratio(Forward P/E / projected annual EPS growth rate over the next 3 to 5 years). Growth-focused investors are willing to pay a premium for future potentials.

Dividend/Income Investing: This strategy focuses on buying stocks that pay regular cash dividends providing investors with steady income while also offering potential for long-term growth. This is popular among risk-average investors who value predictable cash flows. In general, mature and stable companies with consistent earnings return part of the profits to shareholders through dividends usually on a quarterly basis. Companies with payout ratio below 70% are considered sustainable and those with strong cash flow generation can support consistent dividends.

Momentum Investing: This strategy buys stocks that have shown strong recent performance (last 3 to 12 months) under the assumption that the trend will continue. It buys stocks that have had high returns and sells those that have had poor returns. Technical tools like Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Bollinger Bands can be used to identify strong trends. US momentum strategy during 1866 – 2024 period has generated average annual returns of about 9%. However, this strategy is prone to momentum crashes during sharp and sudden market reversals. Risk management is essential for this strategy as momentum strategy had drawdowns exceeding 88% during several reversals.

Low Volatility Investing: This is a defensive equity strategy focused on the stocks with relatively stable price movements, aiming to deliver market-like returns with lower risk. It is designed to protect portfolios during downturns sacrificing some upside during bull markets instead. During crises such as financial crisis in 2008, dot-com bust between 2000 and 2002 and Covid-19 sell-off in 2020, low-volatility portfolio cushioned losses as they were tilted toward defensive sectors such as utilities, consumer staples, and healthcare.

Passive (Index) Investing: This strategy invests in low-cost index funds or ETFs (exchange-traded funds; it is an investment fund that bundles a collection of stocks into one product and trades on stock exchanges) to track a market index (e.g., S&P 500 ETF) rather than picking individual stocks. Passive investing has historically outperformed 80% of active mangers over the long-term.

Active Investing: Active investing strategy attempts to beat the market through security selection and market timing. Bottom-up approach focuses on company-specific research analysing business models, management and competitive advantages and their financials. Top-down approach begins with macro-economic analysis looking at economic trends and policies and then chooses promising regions or sectors before selecting individual stocks.

Core-Satellite Approach: This equity investing strategy combines a stable, low-cost “core” of passive investments such as index funds or ETFs with smaller, actively managed “satellite” positions aimed at enhancing returns. Core portfolio usually accounts for 50-80% consisting of broad, diversified, low-cost index funds or ETFs for stability, long-term growth and reduced volatility. Satellite portfolio has smaller allocation of 20-50%, consisting of actively managed investments, thematic ETFs, sector tilts or individual stocks. This portfolio aims to generate excess returns (alpha). It

is a disciplined approach to combine passive stability with active opportunity making it highly adaptable to different investment goals. Example of core-satellite strategy will be as follows:

Systematic / Factor-Based Investing: It uses quantitative models to identify main factors of stock performance such as quality factor (identify companies with strong fundamentals – high profitability, lower debts, stable earnings and strong management, which provides resilience and higher capital preservation during downturns and lower volatility), growth factor (target companies expected to achieve above-average increase in earnings, revenues or cash flows compared to the broader market – often technology or younger companies with strong growth prospect), momentum factor(invest in winners that keep winning) to construct a portfolio.

Long/Short Equity Strategy: It combines buying stocks expected to rise (taking long positions in undervalued stocks with strong fundamentals) with selling borrowed stocks expected to decline (taking short positions in overvalued stocks) and then repurchasing them at a lower price. This strategy captures alpha from stock selection and tries to profit from both rising and falling stock markets. Net exposure can range from market-neutral, balancing long and short to net-long position depending on investors’ market views.

Event-driven Strategy: This strategy focuses on corporate events. Merger arbitrage profits from the spread between a target’s current price and the acquisition price. Distressed investing buys debts or equities of companies in bankruptcy or restructuring, betting on a turnaround of a company.

Equal-weight Investing: An equal-weight investing assigns the same allocation to every stock in the index, regardless of the size of a company. It reduces the impact of a few mega-cap names dominating in the market-cap-weighted indices such as S&P 500. It provides more balanced exposure across market segments. An equal-weighted investment strategy can outperform market-cap-weighted indices as it avoids concentration risk when large-cap growth falters.

There is no single best equity strategy that works in all conditions. The key is to understand all these investment strategies and build a portfolio that aligns well with your own investment time horizon and risk tolerance.

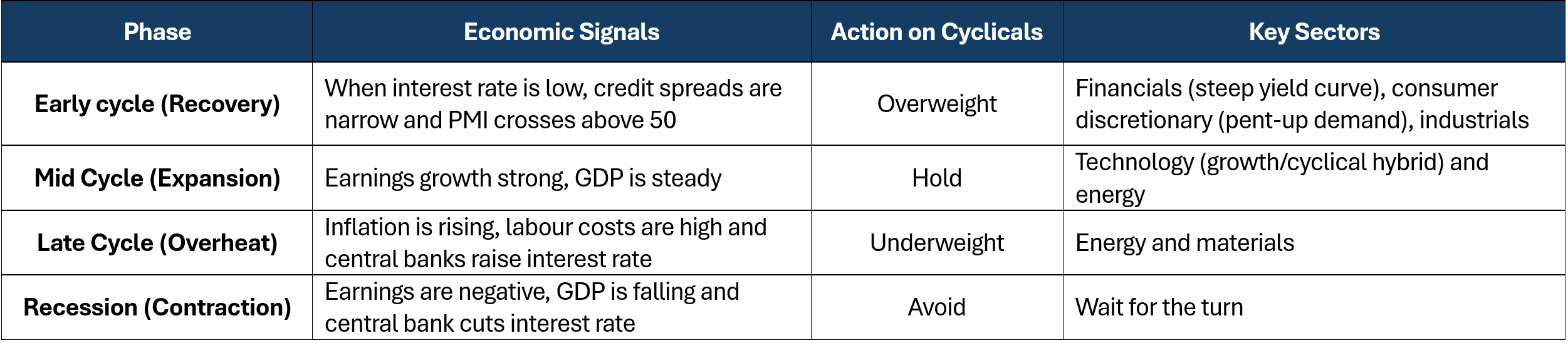

Timing Cyclical Equity Exposure

The performance of cyclical stocks relative to defensive stocks varies according to the stage of the economic cycle.

The performance of cyclical stocks (energy, industrials, materials, consumer discretionary, and financials) relative to defensive stocks (consumer staples, healthcare and utilities) varies depending on the stages of the economic cycle. Cyclical stocks generally lead defensives stocks in periods of economic expansion, while defensive stocks hold up better during downturns.

When ISM Manufacturing PMI is above 50, it is

a buy signal for the industrial and materials sector. When PMI turns up from a

trough (e.g., 48 to 52), cyclical sectors historically outperform the S&P

500 by 15-20% over the next 12 months. Also, peaking initial jobless claims can

signal the end of a downturn and the start of the period to own cyclicals. The

best time to initiate higher cyclical exposure is typically in the 6 to 12

months following a Fed rate cut cycle or a recession scare.