How Effective Is Japan's Currency Intervention?

Yen Interventions Prove Insufficient to Counter the Prevailing Upward Momentum in USDJPY

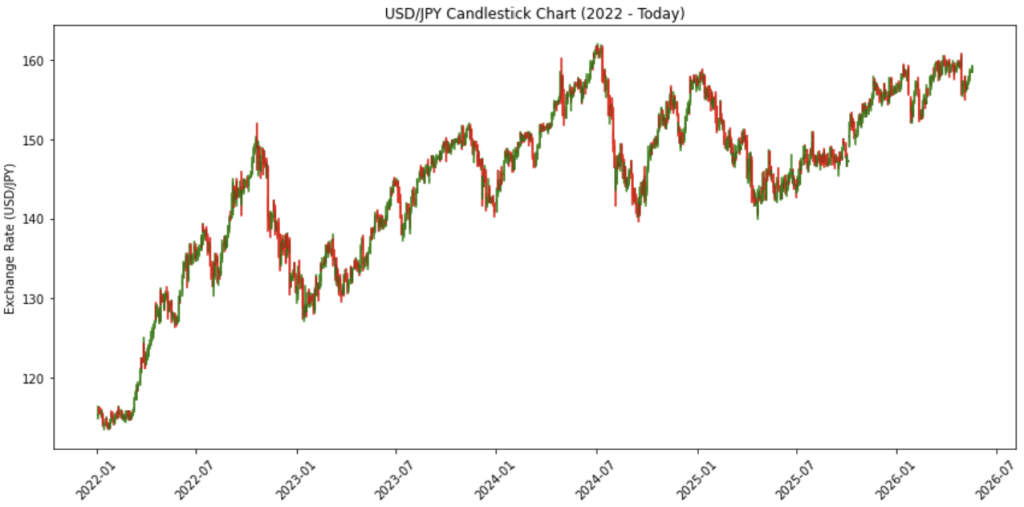

USDJPY

surged past 160.45 on 30 April 2026 prompting Japan’s Ministry of Finance (MOF)

directed intervention (Bank of Japan (BOJ) acted as an agent) to keep USDJPY

below 160 threshold with approximately ¥5 trillion deployed to defend the yen. Additional

interventions followed during the Golden week holidays on 1 May aimed to defend

the 155 level.

Market Impact of Yen Intervention

A sudden change in the expectation of interest rates of US and Japan or a sharp appreciation of the yen can disrupt the yen carry trade — a well-known investment strategy in which investors borrow in low-yielding currency such as yen and invest in high-yielding assets such as US indices or currencies such as US dollar or Australian dollar. Such disruption can weigh on US equity indices including the S&P 500, Nasdaq and Dow Jones. When the BOJ intervenes to support the yen by selling USD and purchasing yen, liquidity will be reduced from the financial system. This action can push the Japanese government bond yields higher adding stress to the Japanese bond market.

Japan holds sizable reserves, with the total reserve assets standing at $1.38 trillion as of April 2026 according to TradingEconomics. However, a large portion of them are invested in securities, so for the effective direct intervention to happen, regulators have to liquidate US Treasury holdings. Should the BOJ decide to defend the yen by selling the

bonds, it could increase volatility in the bond market.

Why Did BOJ Intervene in the Currency Market?

In March and April 2026, the yen slid to the 160 psychological level against USD, driven by 1) Japan’s persistently low interest rates relative to the US’ interest rate (BOJ kept its short-term policy rate at 0.75% in April 2026, while US Federal Reserve kept at 3.50-3.75% range), 2) the widespread use of yen in carry trades, and 3) external pressures

such as surging energy costs due to Iran war (Japan imports about 90% of its energy needs). Even large-scale intervention by Japanese officials only managed to slow down the decline in yen temporarily in the past.

Intensified weakness in yen can impact the broader economy via cost of living crisis as higher energy and food prices can weigh on households’ income and corporates’ margins. Any tightening of BOJ’s monetary policy can amplify the burden of servicing Japan’s vast public debts, which can also worsen fiscal deficits in the country. Based on April 2026 IMF World Economic Outlook data, Japan’s government debt had reached a record amount of $9 trillion, equivalent to 204.4% of GDP – the highest ratio among developed countries (G7). These debts, largely driven by aging population and higher social welfares, are composed primarily of government bonds. Notably, over 88% of them is held domestically with BOJ itself owning around 50% according to the data from Societe Generale.

Higher rates with Japan’s record debt level will make Japan fiscally risky and rising social welfare will continue to push the debt level higher. Higher interest rates will increase the debt-servicing costs as well. To avoid this, Japanese officials chose to intervene in the FX market to curve excessive yen depreciation (to prevent the yen from rising further from 160 psychological level), rather than opting for aggressive rate hikes.

The Era of Defending against Yen Weakness Since 2022

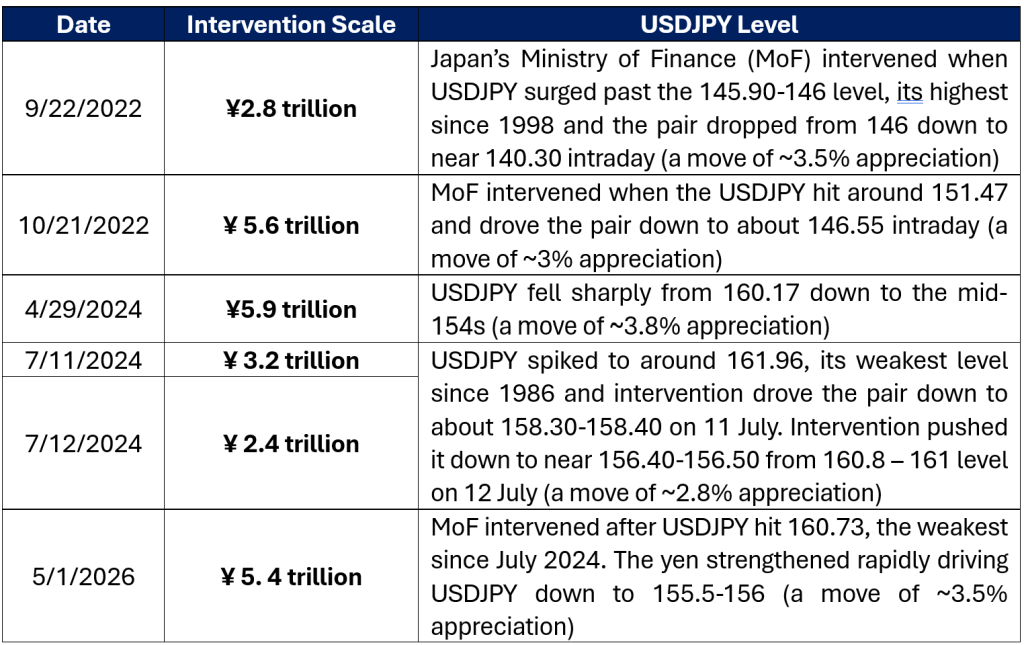

First yen buying intervention by Japanese officials occurred in 2022 since 1998 to prevent rapid depreciation in yen caused by widening interest rate differentials. BOJ intervened in September spending ¥2.84 trillion near 145 level and in October ¥5.62 trillion, with the yen recovering from 151 handle to 146 handle before the dollar’s appreciation against the yen resumed.

In 2022, Fed was in an aggressive tightening cycle to combat the inflation. Fed officials hiked interest rate rapidly from near-zero to 4.75% by the end of 2022. Japan maintained negative interest rates at -0.1% and conducted yield curve control. Yen weakened sharply and Japan intervened in FX markets to defend the yen.

Another intervention happened in April to May in 2024 but this time around, the intervention helped to prompt a reversal in USDJPY trajectory combined with a shift in the expectation of the Fed funds rates and narrowing interest rate differentials between the US and Japan. Compared to 2022 intervention, 2024 intervention shows that Japan’s FX intervention alone can be costly and less effective without US policy support to reverse the trend as global market demand for yen carry trade grows.

In 2024, US rates peaked around 5.25% and then cutting began in late 2024 as inflation moderated. Japan ended negative rates in March 2024 and raised interest rate to 0.25% in July. Yen hit a 38-year low against USD in late April 2024 briefly touching the 161 level. This led Japanese officials to step into the currency market as the yen hit the weakest level since 1986. The depreciation of yen was mainly driven by wide US-Japan interest rate differentials (Fed at 5.25% and BOJ at 0.25%). Yen had been under pressure since 2022 due to BOJ’s ultra-loose monetary policy and until 2024 it continued to face challenges to bounce back from the sharp decline in value.

Fed cut three times in late 2025 and now the current target range is 3.5-3.75%. Fed is cautious to cut interest rates due to geopolitical risk pushing the energy prices higher and hence the inflation higher, while Japan’s policy rate stays at 0.75%. BOJ is signalling further rate hikes but still remained accommodative relative to other central banks. Spread between US and Japan is narrowing due to Fed’s rate cut but unless BOJ delivers a rate hike, interest rate differentials still remain attractive. However, after the FX intervention by Japanese officials, heightened volatility in yen can easily wipe out months of gains from the yen carry trade.

Yen Depreciation Pressure Persisting, Wait for the Next BOJ Meeting

Fundamentally, intervention cannot permanently reverse the trend driven by economic forces such as persistent interest rate differentials. From a technical perspective, the intervention may not have been enough as the USDJPY uptrend off April 2025 low (140.72 on 21 April 2025) still remain intact. April low was a sharp reversal from January 2025 high (158.35). The move in April 2025 reflected narrowing US-Japan interest rate differentials as the Fed began cutting rates in late 2024 while the BOJ cautiously raised interest rates after ending its negative policy.

The yen weakened toward the 160 level in early 2026 due to still wide US-Japan interest rate differentials, persistent carry trade demand (spreads of ~300 bps on short maturities keep US dollar attractive versus yen) and Japan’s structural inflationary pressures. Although BOJ hiked interest rate to 0.75%, US yields still remain much higher even after rate cuts with the Fed funds rates staying at 3.5-3.75% range and 2-year US Treasury yield over 4%. Japanese authorities responded with warnings of “bold action” and intervened to cap USDJPY near 160. However, with the interest rate spread still wide and the Fed expected to keep the rates higher for longer due to higher-than-expected latest inflation figures, yen carry trade still remains profitable continuously pushing USDJPY higher.

JPY depreciation pressure persists given the macro backdrop of elevated oil prices and higher US rates. If Japanese

authorities do not intend to force a sustained JPY appreciation, intervention-defined lows may likely to sit in the mid-155s.

Direct FX intervention still remains likely if USDJPY sustains above 160 and BOJ has signalled possible further rate hikes if inflation remains above target. Investors should note that BOJ hike is necessary for the fundamental support for the yen and to defend BOJ’s credibility instead of officials’ temporarily effective FX interventions.

Key Fundamental Drivers of USDJPY

Risk Sentiment Dynamics: In a risk-on environment, rising equities and positive sentiment drive capital into risk assets including USD and yen often weakens as a funding currency, fuelling a strong bullish move in USDJPY. In a risk-off environment, fear and flight-to-safety dominate. Both USD and JPY act as safe-haven currencies, creating unique and complex behaviour in USDJPY that is less common in other yen pairs. Overall, market participants focus more on global risk sentiment than on interest rate differentials.

Global Risk Sentiment Indicators: Watch S&P 500, Nasdaq and VIX closely. USDJPY typically shows a strong positive correlation with risk assets under most market conditions.

US Treasury Yields: USDJPY and the US 10-year Treasury yield exhibit an exceptionally high correlation (above 90%). Hence, USDJPY is highly sensitive to the movement in the US 10-year Treasury yield. Rising yields generally strengthen the USD, supporting higher USDJPY levels.

Bank of Japan Policy & Intervention: The BOJ’s long-standing ultra-loose monetary policy, combined with occasional

direct currency interventions, often trigger sharp turning points — particularly when USDJPY trads in the 150-160 range.

Technical Levels: Due to heavy institutional and algorithm participation, USDJPY consistently respects major round numbers, prior highs and lows, and key volume profile levels with notable precision.