Europe

July 2026

Fears of prolonged energy supply disruptions promoted bond investors to offload sovereign debts, as higher oil prices were seen as fueling sticky headline inflation and forcing the ECB into continued rate hikes. With crude now back near its pre-war baseline, those inflation concerns have eased considerably. Adding to the oil-driven relief is a weakening macro backdrop that makes it harder for the ECB to sustain its aggressive stance. Although the ECB delivered a 25-basis-point hike to counter persistent price pressures, subsequent data highlight a deteriorating Eurozone economy. Recent indicators, including preliminary PMI figures, show private sector activity slipping back into contraction. As growth falters faster than what policymakers expected, the ECB’s hawkish rhetoric is increasingly colliding with economic reality.

An ECB policymaker emphasized that the Eurozone outlook remains highly uncertain, cautioning that persistent upside inflation risks continue to coexist with downside risks to economic growth. The latest energy shock should not be dismissed as transitory, underscoring the need for monetary policy to remain both flexible and resilient as the economic environment evolves. The primary driver behind the recent bond rally – which moves inversely to yields –

was Brent crude futures slipped below $73 a barrel, fully retracing to levels last seen before the outbreak of the war.

Investors braced for a prolonged “higher-for-longer” rate environment amid potential commodity shocks, triggering a broad sell-off in sovereign debts across the bloc and pushing yields higher. Germany’s policy-sensitive 2-year yield, closely tied to ECB rate expectations, climbed to an intraday peak of 2.877%, its highest since mid-2024, underscoring concerns that persistent sticky energy-driven inflation could keep interest rates restrictive longer for short-end of the curve. At the long-end, the benchmark 10-year yield advanced to 3.137%, the highest since May 20, 2026, as markets priced in a higher term premium to reflect long-term inflation uncertainty. For the Eurozone, a net energy importer, the threat of sustained energy disruption raises stagflationary risks — slowing growth while reigniting consumer price pressures.

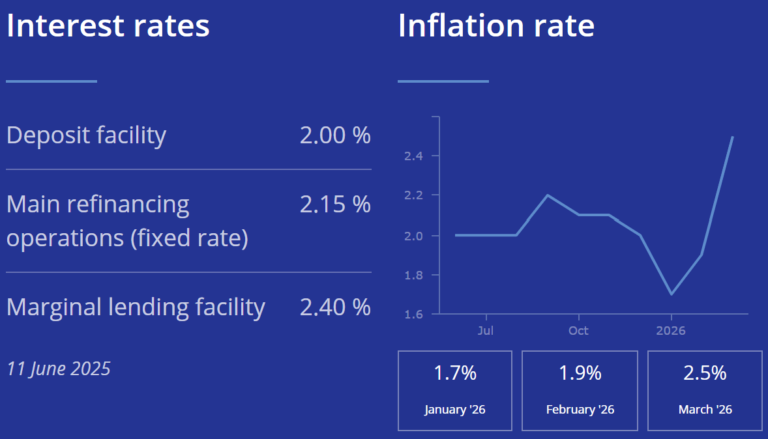

The ECB left its three key rates unchanged at 2.25%, 2.40% and 2.65% for the deposit facility, main refinancing operations, and marginal lending facility, respectively. The pause was widely anticipated after oil prices retreated since the ECB’s June decision to hike rates, easing price pressures. Yet, renewed tensions between the US and Iran

have driven oil price higher again, complicating the inflation outlook. The ECB’s July pause does not signal hesitation. The ECB continues to update forecasts and could raise rates in September. Whether a single hike to 2.5%

will suffice depends as much on growth dynamics as on inflation trends.

Borrowing costs across Europe surged after the ECB warned that “the full inflationary impact of the energy shock has yet to play out”. Shipping disruptions in the Middle East can reignite fears of secondary inflation spikes, lifting yields across maturities. Rising sovereign yields have weighed on equity valuations by increasing corporates’ financing costs and making fixed income more attractive. Rate-sensitive growth sectors remain under pressure, and if oil prices continue their upward trajectory, the ECB may be compelled to tighten further before year-end.

June 2026

On 11 June, The European Central Bank (ECB) raised its three key interest rates by 25 basis points, in line with expectations, as policymakers seek to rein in inflation before higher energy costs caused by Iran conflict spread across the eurozone. The deposit facility rate was lifted to 2.25% from 2%, the main refinancing rate to 2.40%, and the marginal lending facility to 2.65% marking the first increase in nearly 3 years. An ECB executive board member noted that price pressures have broadened beyond energy, increasing the risk of inflation expectations becoming unanchored.

Even if a US-Iran peace deal can curb more pronounced overshoot in inflation, it may not be enough to prevent central banks, including the ECB, from continuing to raise interest rates. The blockade of the Strait of Hormuz has already inflicted significant economic damage, and elevated energy costs are likely to persist longer than many anticipate. Although a peace framework has just been announced, recovery in the Middle East can be slow, as restoring production capacity, rebuilding infrastructure and resuming shipping routes require time.

Within the Economic and Monetary Union, the ECB’s primary mandate is price stability, defined as 2% inflation over the medium term. Yet, inflation is projected to remain above this threshold for several years, despite the tightening cycle between 2022 and 2024, raising concerns that inflation expectations could become unanchored. Importantly, the current surge in inflation is not driven by overheating in Europe, excessive domestic demand or out-of-control wages. Instead, it stems from an imported supply shock: soaring energy prices caused by the conflict in Iran and disruption to maritime routes, which sharply increase costs for business and households. Much of this inflation is imported, reflecting deteriorating terms of trade rather than credit expansion or domestic demand. Meanwhile, eurozone growth is already weak. The ECB projects GDP growth of barely 1% in 2026—far from any sign of overheating. The full impact of earlier monetary tightening is now evident, reflected in tightening financial conditions, a pronounced slowdown in the property market and a contraction in corporate lending.

The challenge of monetary policy lies in the risk that excessive tightening can be just as damaging as premature easing, particularly amid an external energy shock and weak economic activity. By opting to raise rates, the ECB signals that inflation remains as dominant threat, outweighing concerns about stagnation or unemployment. In the context of an imported supply shock, fiscal tools—such as targeted transfers, temporary subsidies, social safety nets, support for the most exposed sector and accelerated energy investment—can be more effective than relying solely on the adjustments to policy interest rates.

May 2026

ECB policymakers warned that the markets may be underestimating the long-term inflation risks stemming from elevated energy costs, renewed supply-chain disruption, and rising inflation expectations. They cautioned that wage pressures can emerge and stressed the need for timely action to avoid being “too late”, reinforcing the expectations that the ECB may remain inclined toward further tightening if geopolitical-driven inflationary pressures broaden across the eurozone economy.

April 2026

The sharp rise in developed market interest rate including Eurozone since the start of the Iran war shows growing concern about higher oil prices fueling inflation, which will drive central banks including European Central Bank (ECB) to tighten monetary policy further in the near term. Oil shock can create a dual impact – on one hand, rising oil prices push up headline inflation driving central banks to maintain or tighten monetary policy. On the other hand, higher energy prices can act as a drag on economic activities, weighing on consumption, pressuring corporate margins and broader growth dynamics. If the shock persists, the focus can shift from inflation control to growth preservation forcing central banks to ease policy later in the cycle as the economic slowdown become a more concern even if inflation remains above target. Policymakers in Europe are expected to maintain a relatively hawkish tone during this ongoing uncertainty provided by energy market.

European economy is more sensitive to oil shocks than the US economy. Oil shock can raise inflation and trim down growth. It is because Europe is an oil importer and larger share of energy accounts for Europe’s consumption basket. As a result, Europe can take a larger hit from this energy shock than the US. When the Middle East tension persists, Europe can face significant price spikes due to lack of gas ahead of winter, which will affect across industrial supply chains and at that stage, demand destruction can happen in the economy. In addition, expansionary fiscal policy (defense, energy, and technology) in Europe can keep rates higher for longer even if the near-term hikes can be proven to be premature despite the on-going energy supply shock from Iran war. Increase in the near-term inflation expectations and worsening growth outlook from the energy price shock increased investors’ bet on interest rate hike by the ECB.

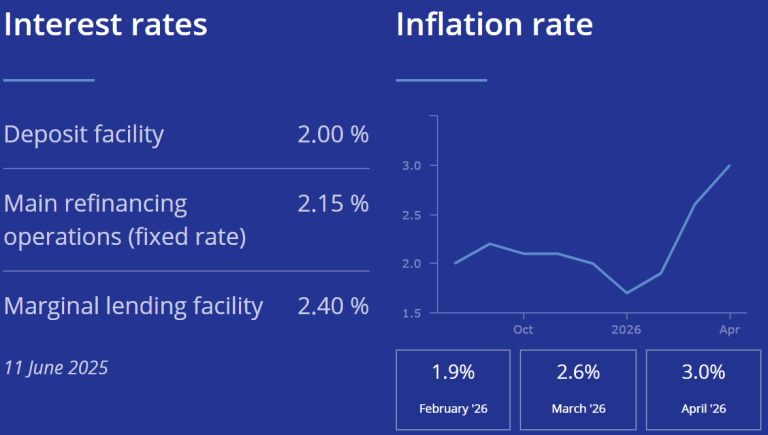

ECB left the three key interest rates unchanged – interest rates on the deposit facility (a pre-set interest rate at which banks make overnight deposit with the ECB), the main refinancing operations (The benchmark policy rate for most lending in the euro area; banks borrow funds from the ECB against collateral, routine funding for banks), the marginal lending facility (a rate at which banks can access overnight liquidity against collateral as the last resort funding when interbank market fails, emergency overnight liquidity and ceiling rate) stayed at 2%, 2.15% and 2.4% respectively. Stagflationary pressure is increasing with weaker-than-expected GDP growth, surging inflation and tighter credit standards in the Eurozone.

Market now expects a rate hike in June from ECB meeting, not driven by

domestic inflation pressures but by the escalating US-Iran conflict and its

impact on Eurozone’s energy prices and supply chains. However, this supply

shock can undermine growth and employment, making aggressive tightening

potentially counterproductive.

March 2026

Geopolitical shock pushed energy and commodities prices higher, which can erode real incomes. On the contrary, easing tensions or improving supply conditions can lower the risk premium and support growth in Europe.

Europe’s growth is improving and inflation is near target and fiscal policies are supportive. However, tariffs, geopolitics and structural issues such as high costs and aging workforce can constrain Europe’s long-term competitiveness. Also, strong resistance to immigration further tightens labour supply, which can worsen due to demographic headwinds.

The European Central Bank (ECB) was more hawkish than the Fed in their latest meeting. ECB was more sensitive to the expectations of modest energy prices amid an economic backdrop where inflation is low, wage growth is moderating and downside risk to growth is genuine. However, early rate hike can run the risk of repeating the policy mistakes made in 2008 and 2011 for Europe (ECB tightened policy into a weakening economy in 2008 and tightened into a sovereign debt crisis in 2011 contrast to the Fed). There is a possibility of a rate hike this year but it remains uncertain how quickly it will translate into action.

February 2026

In Europe, risks have skewed to further easing given the expected undershoot of the inflation target. Appreciation of EUR against USD has also contributed to this. ECB could resume rate cuts in 2026 where EUR strengthens continuously, Eurozone growth is weaker and the inflation is slowing. Between external vulnerability vs domestic resilience, ECB stayed on hold as the domestic resilience dominates for now. But the uncertainty around the monetary policy path has definitely increased.