United Kingdom

July 2026

Inflationary shocks tend to drive a pronounced sell-off at the long-end of the gilt curve relative to the front-end seen in the US and Germany. Whereas rising inflation expectations typically lift short-dated yields and flatten or invert the curve in those markets, the gilt curve bear-steepened, with the long-end absorbing the bulk of the adjustments. This dynamic is largely explained by the term premium, which is the dominant driver of long-dated gilt yields. Roughly two-thirds of the increase in 10-year gilt yields following an inflation shock reflects investors’ demanding higher compensation for holding UK debts (what we refer to as the term premium). That share is notably larger than in the US or Germany, leaving long-dated gilt holders more exposed to outsized mark-to-market losses when inflation surprises to the upside – a risk profile distinct from other G4 bond markets (fixed income markets of the four largest developed economies: the US, the UK, the Eurozone and Japan).

Adding to this vulnerability, nearly one-quarter of the gilt market is inflation-linked, the highest proportion among major developed economies. With about 25% of outstanding supply tied directly to inflation, price shocks feed immediately into debt servicing costs and perceived creditworthiness, amplifying selling pressure at the long end. This elevated share of inflation-linked issuance also explains why the gilt curve steepens not only in response to fiscal risks but also to inflationary pressures from fiscal expansion. Any government spending judged inflationary will impose a double penalty for long-dated gilt investors: wider term premium and higher inflation expectations, reinforcing the market’s tendency toward bear-steepening.

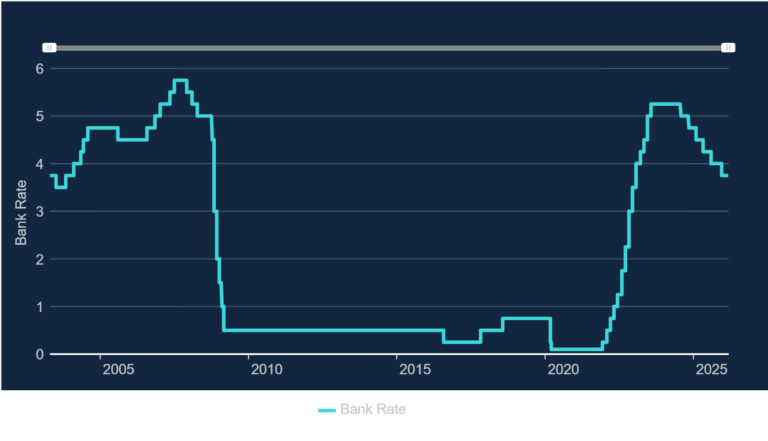

The Bank of England (BOE) held its policy rates at 3.75% but signalled readiness to raise borrowing costs if needed to contain inflationary pressures. The BOE emphasized that while monetary policy cannot directly influence energy prices, it can be calibrated to ensure the economy adjusts to them in a way consistent with achieving the 2% inflation target on a sustainable basis. The appropriate stance, if noted, will depend on the magnitude and persistence of the shock and its transmission through the economy including via financial conditions.

The BOE highlighted that evidence of significant second-round effects in wages and prices remains limited though the risk of such dynamics increases the longer elevated energy prices persist. It warned that risks to the inflation outlook are skewed to the upside and reaffirmed that its readiness to act to keep inflation on track toward 2%. The September meeting is expected to be pivotal, with the balance of risks leaning closer to a potential rate hike.

June 2026

The UK’s fiscal outlook is under strain as rising gilt yields drive up debt-servicing costs. With public debt at roughly 90% of GDP and the deficit still wide, higher yield translates directly into higher debt servicing costs, which without strong economic growth or significant fiscal tightening, can compound quickly. The rise in yields, is not the product of domestic policy missteps but a global phenomenon driven by inflation, with the closure of the Strait of Hormuz and the resulting energy price spike sending bond markets higher across the world. Political uncertainty adds another premium to what investors demand to hold UK debts. In an environment of elevated inflation and higher yields, government finances everywhere are facing sharp scrutiny.

The Bank of England (BOE) held the policy rate steady at 3.75%. Softer-than-expected core inflation and signs of a gradually cooling labor market justified a cautious stance, though the latest employment data appeared somewhat stronger. While interest rates are expected to decline progressively over time, the pace of future rate cuts remain uncertain.

With the ceasefire between the US and Iran, concerns over inflation driven by surging oil prices have eased. As a result, the BOE may not raise interest rates this year, given declining energy costs, moderating inflationary pressures and weakening economic conditions.

May 2026

Yields on longer-dated UK government bonds surged to their highest levels in nearly 30 years, with the 30-year gilt climbing to 5.76%, as investors bolstered their expectations on further interest rate increase from the Bank of England (BOE). The 10-year UK gilt yield also rose to 5.09%, the highest level since late March 2026. BOE warned of higher-than-expected inflation rate while leaving the interest rate on hold at 3.75% in its April meeting. They also mentioned that BOE will need to take action to keep the increase in price under control in the coming months as higher energy prices are expected to spread across to the broader economy.

Yields on UK government bonds have surged to multi-decades highs as political pressure intensified on Prime Minister Keir Starmer to step down. The benchmark 10-year gilt yield spiked to 5.103% with UK bonds selling off across the curve amid heightened uncertainty over the country’s political trajectory.

April 2026

Conflict in the Middle East has triggered a shock to the global economy and it increased risks to financial stability through higher energy prices due to reduction in energy production in the Gulf region. Oil price surged above $100 per barrel, with Brent crude reaching over 60% above pre-conflict level while European and UK natural gas price jumped more than 70% higher versus pre-conflict levels.

Rising energy prices and weakening real income and softening labor market reinforce expectations of the Bank of England (BOE) to remain on hold instead of hiking. Higher energy prices can erode consumer spending, particularly on discretionary items, which can limit the pass-through from headline inflation to core inflation.

BOE left interest rate unchanged at 3.75% and used a more cautious tone without major hawkish leaning. BOE acknowledged that monetary policy cannot affect global energy prices and should look through the initial impact on inflation while second-round effects of inflation (energy-driven price pressure feeding into wages and service prices increasing service inflation) depend on how long energy price remains elevated.

March 2026

An inflationary shock into a weak economy will result in demand destruction and this is unlike in 2021 and 2022 where demand was supported by pandemic stimulus and excess savings. A loose labor market in the UK will make it harder for wage growth to keep pace with inflation, squeezing in real incomes and hitting consumption. Weaker consumers will hit business investments and make the firms more difficult to maintain profit margins unless they pass on higher input costs to consumers.

The long-term positive views on the UK economy – benign balance of payments backdrop, reduced fiscal premium, low energy costs relative to recent years, improved business investment feeding through to productivity – are at risk as conflict drags on and energy costs remain elevated.

Inflation expectation has been a key consideration in BOE’s recent meetings. Anything de-anchoring inflation expectations will likely warrant caution about further easing by BOE. However, a path for further rate cuts remains possible if the energy price shock is short-lived, and does not materially increase inflation expectations. All these factors – disinflationary budget measures set to begin in April, restrictive current rates, downside risk to growth with easing wage growth and weak labor market compared to 2022 energy shock due to Russia’s invasion of Ukraine – support eventual rate cuts instead of a rate hike.

The current economic situation differs from 2022 when Russia invaded Ukraine. Back then, UK’s headline inflation was above 5% and the BOE had begun raising interest rate, having been the first major central bank to hike in December 2021 (It was the 1st rate hike since the start of the pandemic and a surprise move to tackle surging inflation) and interest rate back then was just 0.25%.

Inflation has been declining in recent month on track to reach the BOE’s 2% target, labor market is softening and GDP growth for January was disappointing. Current Interest rate at 3.75% (above 3% to 3.25% range) is considered restrictive. If the geopolitical conflict persists, the base rate is more likely to remain at 3.75% instead of a rate hike.

In rates markets, previously priced-in cuts for 2026 have been unwound following the geopolitical shock, and the outlook for the short-term rates will depend on the magnitude and persistence of energy price moves. The BOE maintained the bank rate at 3.75%, meeting the market expectations. The decision came as the committee assessed inflation implication from higher energy prices amid sluggish economic growth and a cooling job market. UK government bond yields spiked following this decision. Two-year gilt yields rose as high as 4.41% from 4.10%.

February 2026

The UK economy is facing the risk of a recession, which causes a potential for an aggressive policy easing by BOE. Although layoffs are subsided, falling profit expansion could incur more job cuts. Unless there is improvement in jobs data, the UK labor market risk will cause UK economy into a potential recession.

Wage growth in the job market has slowed and service price has normalized, which will help the inflation to go down to the BOE’s 2% target in 2026. In 2025, BOE cut rates by 100 basis points and this year, market expects it to deliver several interest rate cuts.

The rise in unemployment with a notable slowdown in wage growth indicates a further softening in the UK labor market. It suggests potentially increasing pressure on the Bank of England to implement additional interest rate cuts at its next meeting. GBP fell on soft labor market data release.

Disinflation remains intact with the expectation of CPI approaching 2% in spring as the slower wage growth can help temper price increases. Goods inflation is contained, food inflation is falling and service inflation momentum is slowing down. Despite sticky services inflation, weakening labour market would prompt aggressive rate cuts than what the market anticipates with the first cut on March or April and the bank rate can potentially fall to 3% by the end of 2026. The spread between the gilt and swap rates is narrowing, indicating healthy demand for gilts. Risk premium in gilts is disappearing with its yields moving lower.