United States

July 2026

Expectations for a hawkish Fed stem largely from persistently sticky US inflation, with elevated energy prices and rising chip costs adding to overall pressures. Beyond inflation, the labor market remains central to policy decisions. While job growth has cooled, prints have consistently surprised to the upside over the past three months, giving the Fed scope to tighten further. However, June’s decline in gasoline and other energy prices, coupled with softer payroll growth, reduces the urgency for additional rate hikes. On balance, the Fed appears inclined to hold rates steady at its late July meeting.

Under new Fed chair Kevin Warsh, the Fed signaled it would abandon forward guidance to concentrate solely on tackling inflation, given the resilience of the labor market. In public remarks, Warsh reaffirmed his refusal to provide forward guidance, though he acknowledged that inflation risks had eased.

The Federal Reserve faces a critical question: whether the recent surge in energy prices represents a short-term supply shock or a broader inflationary threat. The escalation has reignited fears that higher energy costs could feed

into overall inflation, potentially limiting the Fed’s ability to ease policy despite signs of cooling price pressures. At the same time, AI-relate expenses — semiconductors, memory, electricity — continue to climb even as headline inflation moderates, reinforcing the case for a hawkish stance.

US Treasury yields remain near multi-month highs as crude oil break above $100 per barrel and newly imposed import tariffs intensify concerns about sticky inflation, solidifying expectations that the Fed may raise rates again in September. The 10-year benchmark yield hovered around 4.70%, close to its highest level since January 2025. The

2-year yield stayed elevated near 4.32%, while the 30-year yield held above 5.10% — its longest stretch above 4% mark in two decades. Bond yields rose across the curve after oil price spiked on threats of military action in the Middle East shipping lanes and the immediate rollout of US import tariffs ranging from 10% to 12.5%.

Persistently high yields carry significant macroeconomic consequences. With borrowing costs at multi-year peaks, the US government faces steep interest expenses as it refinances maturing debts and funds widening fiscal deficits, adding structural pressure to long-term yields. Treasury yields also anchor commercial rates across the economy: mortgage costs have climbed back toward multi-month highs, dampening housing activity, while corporate financing costs have risen alongside energy input prices. This dual squeeze on profit margins threaten to slow capital expenditure and private investment in the second half of the year. Elevated borrowing costs function as a structural

drag on economic growth, leaving the financial market increasingly vulnerable to the twin headwinds of high-yield environment and energy-fuelled inflation.

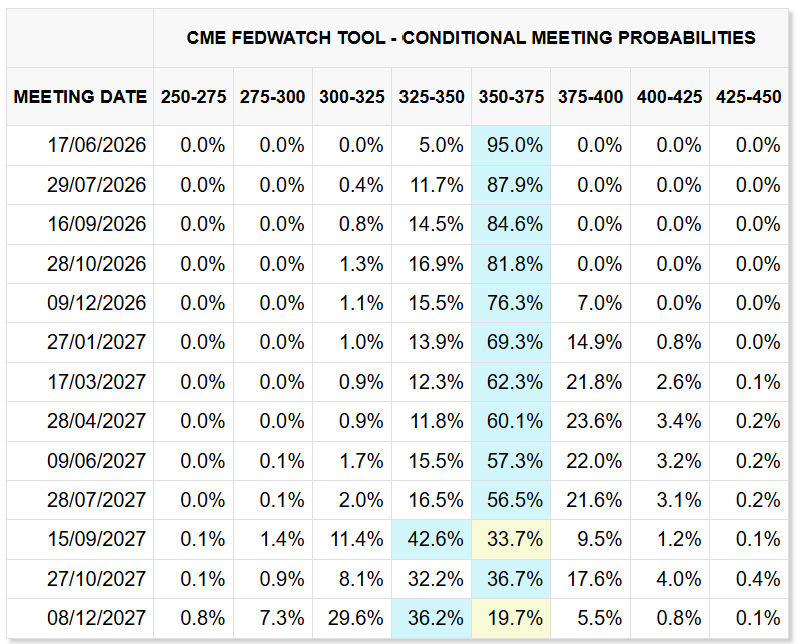

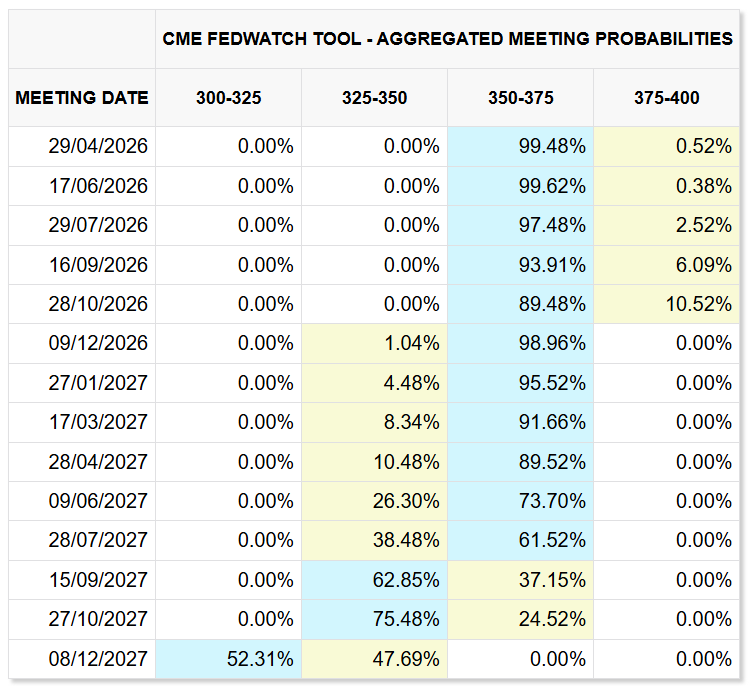

The Federal Open Market Committee (FOMC) left the federal funds rate unchanged at 3.5%-3.75% for the fifth consecutive meeting. While this outcome was largely anticipated, the probability of a rate hike had risen above recent norms amid rapidly shifting inflation pressures driven by volatile oil prices.

Notably, rising US Treasury yields has effectively played the role of a rate hike, as an increase in yields usually raise borrowing costs for consumers and businesses. Since the Fed’s June meeting, the benchmark 10-year Treasury yield has climbed more than 14 basis points. According to the Fed Chair, the Treasury market appears to be reflecting strong US economic output, robust capital expenditures, steady productivity gains and a resilient labour market.

June 2026

The US debt-to-GDP ratio exceeds 100%, currently around 121%, highlighting how much a country’s borrowing weighs on its economy. With interest rate still elevated, servicing this debt has become increasingly costly. National debt stands at $39.18 trillion as of 28 May 2026, and mounting fiscal pressures have weighed on the Treasury bonds, while inflation concerns have recently triggered a sell-off. Over time, the debt burden can contribute to a downward pressure on the USD.

The recent climb in the 10-year Treasury yield to 4.67% was driven less by growth expectations and more by concerns over Treasury supply and widening government’s fiscal deficits. Now that those supply fears have eased a bit, yields have moved lower again. Bond markets remain anchored on slowing growth and moderating inflation, though heightened geopolitical risk is adding volatility. The ongoing Middle East conflict has lifted energy price and inflation expectations, feeding directly into higher long-term yields and mortgages rates, which in turn are weighing on the US housing market. Investors have scaled back expectations for the Federal Reserve rate cuts this year, and some analysts now see that persistent energy-driven inflation could even reopen the door to another rate hike.

At the Fed’s meeting—the first under the new Chairman Kevin Warsh—the Federal Reserve kept interest rates unchanged within the 3.5% to 3.75% target range. Wash abstained from submitting a projection, adding uncertainty to the forecast. His remarks struck a distinctly hawkish tone, emphasizing repeatedly the Fed’s commitment to price stability. Treasury yields climbed in response, with the 2-year yield surging more than 16 basis points to 4.216%.

May 2026

US 10-year Treasury yields have climbed to 4.54%, the highest since May 2025, while 2-year yields have also surged back above 4%. Despite equities rallying for several consecutive weeks, the bond market continues to signal concerns over inflation and a deteriorating global economic outlook.

Long-bonds priced in higher inflation expectation and higher Treasury supply. Sticky services costs, resilient wages and fiscal stimulus have been keeping the inflation expectation elevated. On the supply side, US is financing structurally large deficits (interest costs, entitlements and elevated outlay from an ongoing Iran conflict). As a result, much longer-dated bonds are due for auctions. Many foreign buyers have remained on the sidelines in recent years as has the Federal Reserve since they halted the quantitative easing program in 2022. Also, the acceleration of the AI narrative is attracting global investment capital away from the safety of US Treasuries. As a result, 5% can be a floor not a ceiling for 30-year US Treasury bonds unless inflation softens materially or the deficit shrinks.

Fed officials cautioned that interest rates may need to stay on hold for an extended period of time. They also note that the ongoing conflict in Iran could create more persistent inflation pressures while simultaneously dampening the growth in the economy with increasing risk of stagflation. No longer the Fed is expected to cut rates this year with the terminal rates (the peak level of the benchmark interest rates before policymakers halt hikes or start cutting rates) stays at 3.0-3.25%.

Investors remained concerned that sustained higher energy costs could keep inflation high and potentially reignite inflation expectations, with secondary effects spilling over into other goods and services. Against this backdrop, US Treasury yields moved higher across the curve with the 2-year yield rose above 4%,10-year yield climbed past 4.5% and the 30-year yield held comfortably above 5%.

A bear steepening of the yield curve has not historically served as a reliable signal for equity sell-offs and on average, has been followed by positive equity performance. While short-term drawdowns can occur as markets adjust to a higher-rate environment, the broader uptrend often resumes. Elevated rates do not necessarily derail bull markets when economic growth remains robust. Despite rising yields, the equity rally is well-supported by strong global government spending (With the US, China, Germany, and Japan — together accounting for more than half of global GDP — still in fiscal expansion mode), resilient consumer demand (April retail sales up 0.5% month-over-month) and significant corporate investment in AI infrastructure (data center capital expenditure running at 2.5% of US GDP and still rising). Household and corporates and government are spending, continuing to underpin equity prices. While higher mortgage rates may weigh on consumer activity, they are unlikely to curtail government spending already approved by the Congress or ongoing AI-related corporates’ capital expenditure.

April 2026

The key variable for policymakers has been long-term inflation expectation (if it is anchored or not) not the headline inflation. Headline inflation is the raw inflation figure measured by Consumer Price Index, which reflects the direct cost-of-living impact on households and it is often more volatile than core inflation. Headline inflation has been pushed higher by energy prices and as a result, short-term inflation gauges such as one-year inflation expectation, have risen but long-term inflation expectations have stayed relatively stable. This reflects temporary energy-related price pressures rather than a structural shift in inflation dynamics. As there is limited pass-through from higher oil prices to core inflation (which excludes volatile food and energy components), Fed may look past the current spike in

energy prices.

Financial conditions have tightened due to higher oil prices since the start of the Middle East conflict and combined with a stronger dollar, equity risk premium was pushed up having the same effect as rate hike. This tightening reduces the need for additional policy tightening from the Fed. As a result, this oil shock may not change the Fed’s easing trajectory in the second half of 2026 as growth moderates and inflation gradually cools down. If the central bank delivers two 25-basis-point cuts, the policy rate will be brought down to 3.0% to 3.25% range (from 3.5% to 3.75% range). However, as energy shocks feed into broader price-setting, there could be a sustained rise in long-term inflation expectation. In that case, Fed will be forced to keep the interest rate higher for longer or even consider a rate hike.

Monetary tightening works on the demand side so a supply shock cannot be fixed with monetary policy. Rate hike can rather exacerbate the slowdown in the economic activity potentially leading to a recession or a stagflation. Every

recession since World War II, except for the Covid-19 pandemic, was preceded by a jump in oil prices. Rising oil prices, an unsustainable tech capex boom, high home prices and stresses in private credit are all contributing to the risk of recession.

A strong rebound in employment in the US suggests that US economy is relatively in a decent shape to weather the economic headwinds coming from the Middle East conflict. However, job creation remains concentrated in handful of

sectors and rising uncertainty can make employers more hesitant to accelerate their hiring plans. Federal Reserve seems to be comfortable with maintaining its current policy, with steady growth and resilient labor market suggesting

the expectation of near-term easing can be premature.

Kevin Warsh, Trump’s nominee for Fed Chair mentioned that he had made no commitments to cut interest rates and put an emphasis on the central bank’s independence and shrinking Fed’s balance sheet. Prolonged disruption in the

energy market can force the Fed into monetary policy tightening. The Fed kept its policy rate at 3.5% – 3.75% in its April meeting as widely expected and focused on inflationary effect of the Iran conflict.

March 2026

10-year Treasuries continued to go higher as oil prices stay elevated, inflation fears continued to outweigh safety demand for US bond market. Investors continued to weigh inflation fears more than safety flow.

The spike in the US oil price is lifting inflation expectations that could put consumer spending under pressure. The recent rise in oil price has been weighing on the stock market. Investors remain in risk-off mode as worries grow over on the duration of the conflict and potential disruption of energy supply.

Escalating geopolitical tensions and fears of energy supply disruption continue to dominate market narratives with the crude oil price continued to run higher. US Treasury yields were mixed with shorter-end moving lower on the expectations that the Fed may need to ease due to slowing economy. Longer-end moved higher on the back of higher inflation risk.

The Federal Reserve left rates unchanged (at the 3.5% – 3.75% target range) after the latest meeting due to uncertainty around the trajectory of the geopolitical conflict between US-Israel and Iran. However, they did not change their projections for the rates this year signalling there could be a rate cut, which puts Fed in the position as the only major global central bank not anticipated to raise rates in 2026 to combat the inflation.

February 2026

Higher inflation has created a conundrum for the Federal Reserve to decide whether to cut interest rates for growth or to hold steady to continue to fight inflation. It creates uncertainty around which way the policy is going for the rest of the year. Although job growth was much better-than-expected last month, layoffs have been picking up making doubtful about the stabilization of the labor market.

Equity market struggled which shows a sign of stress building beneath the surface of financial markets as the sentiment soured. Nasdaq got lower for the month highlighting continued pressure on valuation-sensitive sectors. Dow, however, showed relative resilience as investors rotated towards more defensive and cyclically stable sectors amid sticky inflation.

Rising inflation expectations can cause a spike in long-term Treasury yields, and potentially a pullback in stock valuation. Weaker job data and safe haven demand could push the 2-yield rate lower, but the combination of stronger US economic data and weaker auction demand ($60 billion 20-year Treasury auction) reinforced long-end yield moving higher underpinning USD.

President Donald Trump nominated Kevin Warsh to serve as the next Fed Chair pending the Senate’s confirmation. He would succeed Jerome Powell who will end his term in May 2026. Despite his hawkish voices during his prior time at the Fed, Kevin Warsh is currently in favour of policy easing in 2026, due to productivity gains fuelling economic growth without necessarily moving up the inflation higher, allowing the interest rate to come down.

Monetary policy is set to balance between the risk of higher and persistent inflation and the risk of weaker labour market and household spending. Current Fed funds rate at right around neutral implies policy is neither restrictive nor stimulative at this stage. When the labour market is stable, inflation is still above the target, there is no urgency for the Fed to cut rates. Fed has signalled no urgency to cut unless labour conditions deteriorate materially. Policymakers seek clearer evidence of disinflation before backing lower rates.

US fiscal deficit is on a structurally upward trajectory with deficits projected to remain high through the next decade. The deficit is expected to hit approximately $1.9 trillion in fiscal year 2026 driven by mandatory spending (Medicare and social security) and rising interest costs (net interest cost is projected to surpass $1 trillion annually).

US has persistently high deficits which are expected to rise from 5.8% of GDP in 2026 to 6.7% in 2036 higher than the 50-year average of 3.8%. US general government debt to GDP is around 121% ranking among the highest around the world. US is one of the top-tier indebted countries, behind only Japan (236%) and Italy (135%) among developed economies as of early 2026.

The high US debt ratio is primarily driven by sustained budget deficits (government’s spending exceeds the revenue, money that the government collects), Covid-19 pandemic spending, and an aging population. Emerging economies such as China and India have relatively lower debt, but they also have seen rising debt to GDP ratio.

The 2025 “One Big Beautiful Bill Act” and immigration policy are expected to add around $5.2 trillion to deficits over the next decade. Although the tariffs would reduce the deficit around $3 trillion over 10 years, these are not enough to offset higher spending.