What Are Economic Cycle and Credit Cycle?

What Is Economic Cycle?

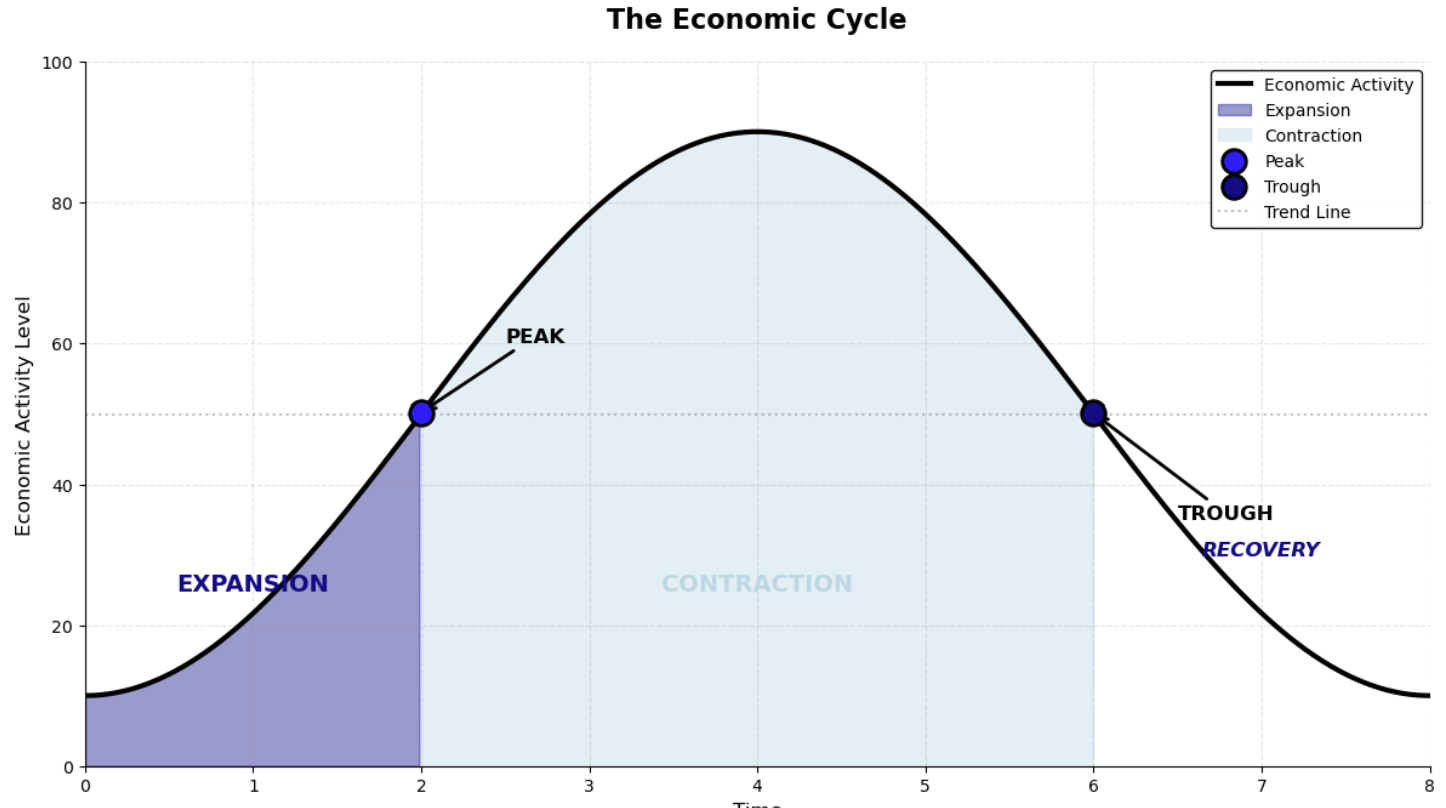

There are 4 main phases of the economic cycle.

Expansion (Growth): The economy grows positively in this cycle with increasing GDP (producing more goods and services). Businesses generally hire more people to meet growing demand. The economy has low unemployment and increasing business investment. Consumer confidence generally rises and consumer spending also increases. As demand grows, prices begin to rise but at a manageable inflation rate. It shows a virtuous cycle of spending, hiring and producing.

Peak: this is the height of the expansion with the economy running at its full steam and growth rates at their maximum. It’s a turning point. The economy is already producing at its full capacity (maximum output) and the economy is at full employment. With the demand outstripping supply, prices rise rapidly with the signs of high inflation. The economy shows a sign of being overheated. Asset prices including housing and stocks can be overvalued at this stage.

Contraction (Recession): It is a downturn and the economic growth slows down and then turns into negative with the economy shrinking with the falling GDP. Businesses face falling demand and they began to lay off workers and stop hiring, which causes rise in unemployment. Consumer confidence falls and being fearful of the future, people save more and spend less. Business investment decelerates with falling inflation (disinflation) or deflation as the demand dries up with the prices stagnate or even falling. This is a vicious cycle of reduction in consumer spending and job losses. A severe and prolonged contraction in this stage is called depression.

Trough: This refers to the lowest point of the economic cycle. The economy hits the bottom and prepares for a recovery. Economic indicators show the economy is bottoming out with joblessness and unemployment rate at its peak. Factories and resources are still at low capacity utilization rate and business have excess inventories. However, from here the economy will be led back into the expansion phase.

Causes of Economic Cycle

Demand and supply: It can be because of changes in consumer spending, business investment or external factors such as sudden spike in oil prices which triggers a shift in the stage of the economy.

Monetary policy: Central banks influence the cycle through raising interest rates in order to cool down an overheated economy or lower the interest rates to stimulate a sluggish economy.

Fiscal policy: Tax cut or increased government spending can boost the economy while austerity measure will slow down the economy.

Market psychological factors: The collective psychology of consumers and businesses – optimistic or pessimistic views – can become a self-fulfilling prophecy driving the economic cycle.

Innovation and technological advancement: Major new technology such as the development of the internet or AI can spark a long period of investment and expansion of an economy.

Economic Indicators

Some data points are used to track where we are in the economic cycle.

Leading indicators: Leading indicators tend to change before the overall economy shifts, helping to forecast future economic activities. Stock market performance or stock market returns as the prices reflect future expectations, ISM manufacturing index, PMI data, building permits signalling future construction, consumer confidence index reflecting future spending, yield curve – the spread between long and short-term interest rates can help to predict the future of an economy’s performance as a leading indicator.

Coincident Indicators: Change happens at roughly the same time as the overall economy shifts, which can provide real-time insights into the current state of the economy. This includes GDP, industrial production, personal income, employment, payrolls and retail sales.

Lagging indicators: Lagging indicators change after the overall economy has begun following a new trend. They usually confirm long-term patterns or turning points. Lagging indicators include unemployment rate (rises well after a recession starts and falls after recovery began), corporate profits (reported with a delay), interest rates (central banks often change rates after inflation or growth shifts), consumer price index (inflation trends lag money supply or policy change) and outstanding bank loan delinquencies (peak after a recession ends).

Secular trends: A secular trend refers to long-term, fundamental shifts in the economy that can last for decades and short-term business cycles can ride on it. For instance, an aging population is a secular trend that can affect developed nations in general.

What Is Credit Cycle?

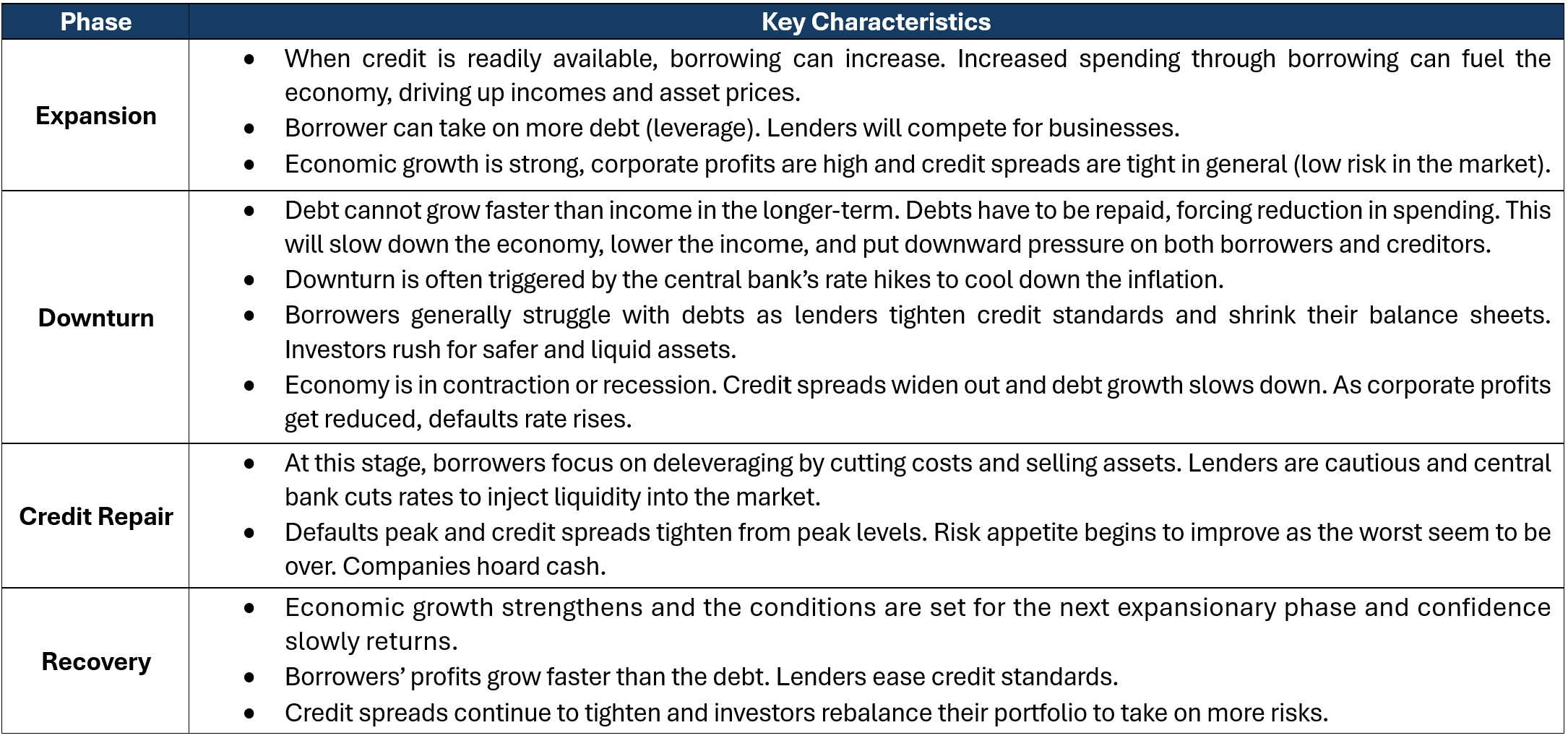

Credit cycle can describe how debt drives the economy in repetitive patterns. Ray Dalio (an American billionaire investor and an author known for founding Bridgewater Associates, one of the largest hedge funds in the world) explains that credit cycles are inevitable as they stem from basic human nature and mechanics of borrowing.

Short-term debt cycle (5 to 8 years): this is similar to “business cycle” of boom and bust driven by central bank’s policies (either raising interest rates or lowering interest rates). These refer to regular expansions and recessions seen every few years.

Long-term debt cycle (50 to 75 years): Each short-term cycle ends with debt levels higher than before and as a result, debt accumulates over decades. This is a big cycle where this long-term cycle ends up with heavy debt burdens that traditional interest cuts can no longer stimulate growth.

Late stage of a long-term debt cycle needs to be addressed as a major debt crisis can hit. Policymakers usually have 4 levers to address it and deleverage the economy: 1) austerity (reduction in spending), 2) debt defaults or restructuring, 3) printing money (monetary expansion), 4) wealth transfer (from the haves to the have-nots). The ideal situation is when these tools are used in a balanced manner so that the debt burdens fall while economic growth and inflation remain intact. The worst outcome would be a depression or hyperinflation.

Why Credit Cycle Matters?

Credit can amplify economic swings. During expansions, for example, easy access to credits can fuel spending and investment, pushing growth higher. When credit is abundant, money can flow into assets such as stocks, real estates, and bonds driving up the prices. During downturns, however, the lack of accessible capital can force companies into bankruptcies deepening a recession and asset prices can collapse as credits dry up.

Historical examples include 2008 global financial crisis, Lost Decade in Japan, and the Spanish real estate crisis, which were born from excessive credit expansion followed by a sudden, painful contraction. Some studies on historical data prove that economic downturns associated with credit crunches are more severe than regular recessions as GDP is significantly damaged by credit contractions but not boosted by expansions significantly.

How to Track Credit Cycle?

There are several indicators to track credit cycle.

Central bank policy: The primary driver of credit cycle is interest rate decisions made by central banks. Rate cuts can stimulate the economy through abundant credits, while rate hikes can cool down an overheated economy.

Credit-to-GDP gap: This measures the current level of credit in the economy against the long-term GDP trend. A large positive gap means credit is growing much faster than its historical average relative to GDP signalling an overheated economy with potential vulnerability.

Credit spreads: This refers to the difference in yields between the corporate bonds and government bonds. Tightening spreads suggest confidence in the market and stronger risk appetite, while widening spreads indicate growing fear in the market and a flight to safety.

Lending standards: Surveys from bank loan officers can show if credit is becoming easier or harder to obtain and this can be a leading indicator of the credit cycle’s direction.